![]() Why you can trust The Zebra

Why you can trust The Zebra

Susan is a licensed insurance agent and has worked as a writer and editor for over 10 years across a number of industries. She has worked at The Zebr…

- Licensed Insurance Agent — Property and Casualty

Ross joined The Zebra as a writer and researcher in 2019. He specialized in writing insurance content to help shoppers make informed decisions.

Ross h…

- 5+ years in the Insurance Industry

Should you buy life insurance in your 20s?

If you're like most young adults, purchasing a life insurance policy probably isn't at the top of your list of things to do in your 20s. Although early adulthood may be the perfect time to do fun and exciting things like travel the world or move to a new state, it’s also one of the best times to invest in your future and lay the groundwork for your legacy. One way you can set your future self up for success is by getting life insurance.

Investing in life insurance as a young adult can help you plan for future finances and ensure your legacy in case of the unexpected. Additionally, obtaining a policy while you’re young and healthy will help you lock in coverage at lower premiums. Despite the benefits it can offer, many 20-somethings may find it hard to justify an added monthly or annual expense for which they won’t get an immediate return. If you’re considering getting a policy in your 20s, read through this guide for scenarios in which life insurance is beneficial and reasons why it’s useful to get it young.

Don’t forget to jump down to the infographic for additional ways to invest in yourself and build a brighter future.

Benefits of buying life insurance early?

Buying life insurance in your 20s puts you in the best position to obtain a lifetime of coverage with a much more affordable premium. Although this can be very advantageous, the decision to purchase a policy young is dependent on your current goals and financial situation. For more insight on whether life insurance is worthwhile for you, check out the different circumstances when it may or may not be beneficial below.

When life insurance may be beneficial for 20-somethings:

- If you have a family or are planning to have a family in the future

- If you have individuals who are financially dependent on you

- If you owe money (student debt, mortgage, etc.) that may leave a financial burden on family

- If you’d like to ensure coverage in the event you develop a chronic illness or condition later in life

- If you generate excess income and need additional places to invest your money

When life insurance may not be beneficial for young adults:

- If you’re financially stable, have no debt or possess enough savings to cover your debts and any other financial burdens in case of your death

- If you never plan on having a family or other financial dependents

- If you can’t currently afford to pay additional expenses such as a life insurance premium

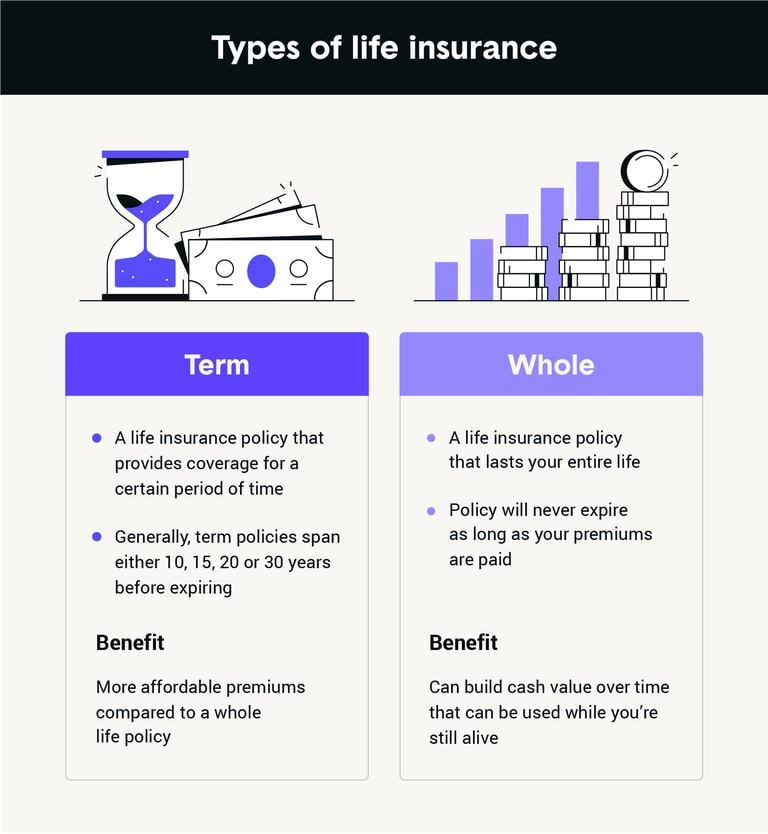

Term or whole life insurance: Which is better for young adults?

If you decide that it’s worthwhile for you to purchase life insurance young, you’ll have to choose between a term or whole life insurance policy. Term life insurance covers you over a certain span of time and typically covers periods of 10, 15, 20 or 30 years. On the other hand, whole life insurance is a permanent form of coverage that never expires (unless you stop paying your premiums).

Whole life insurance also has the ability to grow cash value over time. This is an advantage compared to term policies, but premiums tend to be significantly higher. However, whole life policies also have the added benefit of allowing you to withdraw funds from this cash value when you need it.

Out of the two types of life insurance, the best option for young adults will likely be a term life insurance policy. While a whole life policy certainly has the added financial benefits of cash value, the extra costs of this type of policy are not likely to make this the best option for younger adults. Those looking for an investment vehicle will likely find better returns through other options. A term life insurance policy will provide a solid financial cushion for most young people in the event of their passing.

Eight reasons to get life insurance young

To help you decide whether obtaining life insurance in your 20s is right for you, we’ve compiled a list of eight reasons why getting a policy early will be worth your while.

1. Obtain coverage easier

When you decide to purchase life insurance while you’re young and healthy, it’s often much easier to obtain coverage. Although most companies will ask for a medical exam before obtaining coverage, some companies won’t if you’re a healthy young adult. In fact, you may just need to answer questions about your medical history before gaining coverage. Many companies are making the online purchase of life insurance easier and quicker than ever.

Additionally, if you’re healthy with no pre-existing conditions, you won’t have any difficulties getting covered or potentially being denied coverage. As you age and your health naturally deteriorates, it can be harder to get insured.

2. Enjoy a quicker buying experience

Getting life insurance early can also mean a better buying experience. Life insurance companies often have faster processes if you’re purchasing young. Certain companies may not require a medical exam and may also allow you to answer questions over the phone before getting coverage.

This results in a much quicker and more efficient coverage experience, and it will save you time if your life gets busy with your career, a growing family or other responsibilities later. If your needs ever change, it’s possible to customize your coverage after purchasing, and you can learn more about this in the next section.

3. Pay lower premiums

Another benefit to investing in life insurance early is that you’re more likely to lock in a lower premium. Premiums for 25-year-old adults in good health are typically much more affordable than if you were to begin coverage at 40 years old.

Additionally, if you wait until you’re older and potentially develop a chronic health condition, your premiums will be more expensive due to your more complicated health record. It’s helpful to secure an affordable premium early because it will be difficult for life insurance companies to change your rate should you develop an illness or other health condition later in life.

4. Provide a safety net for family

If you have loved ones that you want to make sure are taken care of, life insurance can help provide financial support in case the unexpected should happen to you. Whether you want to name a spouse, children, parents or siblings as the beneficiary of your policy, it can help cover any financial burden they might experience in your absence. For those that plan on starting a family in the future, a life insurance policy will be a good investment to have now that will come in handy when you are responsible for raising and supporting a child.

Also, life insurance will help safeguard your family’s finances in case you pass and have unpaid debts. Debts like a mortgage or student loans may leave your family on the hook for repayment after you’re gone. Additionally, some community property states will consider you and your spouse equally responsible for the debt, so creditors may hold them accountable. A life insurance payout can ensure that your family won’t have financial struggles on your account and that they won’t ever have to worry if creditors come calling.

5. Begin your legacy

As a young adult, it’s likely that you haven’t amassed great wealth yet. For most people, wealth generation takes time and careful years of planning. If you want to make sure that no matter the size of your savings account or investment portfolio, you have something to pass on to your family — life insurance can help you do this.

6. Benefit from flexibility later

Once you’ve secured a life insurance policy, you'll have much more flexibility when it comes to updating it. Whether you opt for a term or whole insurance policy, you can purchase life insurance riders to gain coverage for specific circumstances. Riders allow you to customize your coverage, much like a home or auto insurance endorsement.

A common rider option is a waiver of premiums, which waives payments in case you become disabled or a chronic illness prevents you from working. Other examples include family insurance riders, accelerated death benefit riders or long-term care riders. For more information on these options, head over to our life insurance rider guide.

7. Build your investment over time

One advantage of obtaining life insurance as a young adult is that if you choose a whole life policy, it has the potential to generate cash value. Any premiums you pay toward whole life insurance not only go toward the death benefit that will be paid out to your beneficiaries, but also work toward building a cash value account. This cash value can be used while you’re still alive in case you need the funds.

Cash value accounts are a relatively low-risk investment opportunity, as some options are protected from fluctuations in the market, unlike stocks. Since a whole life policy never expires, you can count on this money to be there when you need it or to go toward your loved ones after you pass. Because a cash value account grows with time, the earlier you start investing in it, the more you and your loved ones can benefit financially from it.

8. Invest your excess income

If you’re a particularly high earner, you may be looking for additional ways to invest your hard-earned cash. Investment accounts like 401(k)s and Roth IRAs have a maximum you can contribute to every year, but you may not feel comfortable putting your extra money into riskier investments in the stock market. Whole life insurance comes with a cash value account that serves as another safe place to invest and grow your excess income.

Overall, there are many good reasons to invest in life insurance as a young adult. Whether you plan to provide for your loved ones or want to begin building your financial legacy, a life insurance policy can help you reach your goals. Consider your particular circumstances and weigh the benefits listed in this guide so that you can make the decision that is right for you.

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.