Minnesota SR-22 insurance

An SR-22 is a routine legal requirement triggered by a violation such as a DUI conviction, a ticket for driving without insurance, an at-fault collision, driving with a suspended license, or accumulating too many points on your license. It is not a type of insurance policy, but a form issued by your insurance company with the state of Minnesota to ensure that you remain insured.

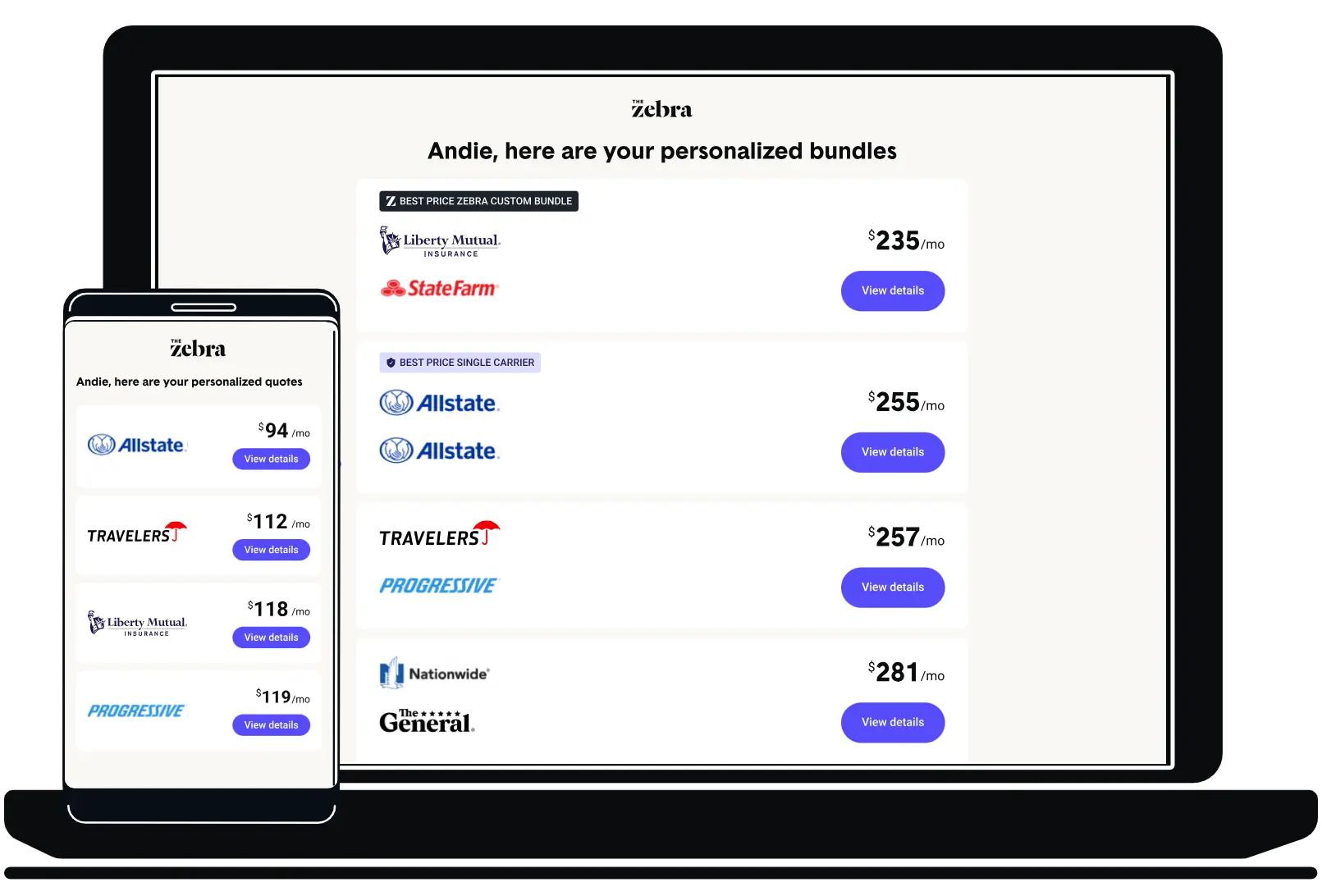

Finding cheap auto insurance with an SR-22 in Minnesota might require some research, but it could pay off in the end.

How to acquire an SR-22 in Minnesota

For currently insured drivers

If you already have auto insurance, getting an SR-22 certificate is straightforward. Contact your car insurance company ask the company to file an SR-22 request for you. If your insurer isn’t willing to file a request, you'll need to look for a new insurer.

For uninsured drivers

When filing for a new policy, you might be saddled with an up-front fee to have your prospective insurer file an SR-22 request for you and to cover your high-risk driving profile. Needing an SR-22 might disqualify you from purchasing insurance from some companies, while others would be happy to sell you a policy.

For drivers without a vehicle

Not owning a vehicle makes it more difficult to obtain an SR-22, as you will need to furnish proof of insurance to receive the certificate. In this scenario, purchase a non-owners car insurance policy before filing an SR-22 request. Non-owners auto insurance is typically less expensive than traditional coverage since it doesn't protect against material damage to your vehicle.