Every day, Americans struggle with major financial decisions. Juggling large payments on top of recurring debt can be overwhelming, making the cheap upfront cost of leasing a car an attractive option. While leasing may seem more affordable than purchasing a used car, there are long-term considerations not immediately apparent when making that first down payment.

Follow along for a better understanding of what is exactly involved in leasing a car, in regards to three factors: monthly payments, control over the vehicle, and maintainence.

- What it means to lease a car

- Payments

- Customization/control of the car

- Maintainence

- When's the best time to buy or lease a car?

- Leasing vs buying a car with bad credit

- Leasing vs buying a car for rideshare

- Summary

How to lease a car

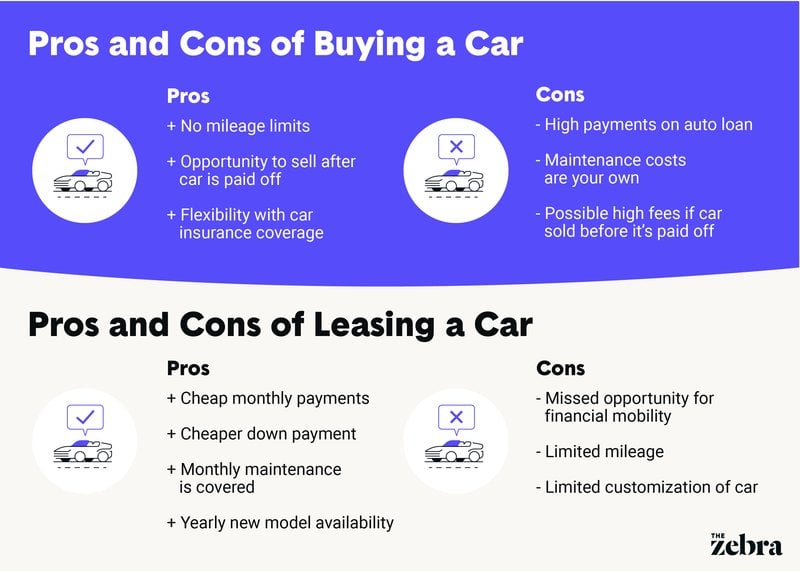

Leasing a car simply means you are renting the car temporarily, with the intention of bringing it back at the end of your lease. Leasing a car is similar to renting a house or apartment — with the same primary benefit: monthly lease payments are much cheaper than paying to purchase the item. When leasing a car, payments come out to approximately 20% of the car’s purchase price. The dealership calculates these payments based on the driver’s credit score and the amount of the original down payment, so not all lease payments are equal.

Vehicular leases usually last three or four years, so be sure to save up for another down payment in addition to the monthly car payments. At the end of the term, you can purchase the car outright for the calculated buyout price, or turn it back in.

Leasing vs Owning a Car: Comparing Payments

If you're on the fence between leasing and owning a car, there are a few benefits to consider. The biggest bonus of a lease is not fronting the immediate expense of a new vehicle. With a good credit score and consistent on-time payments, and you can drive a new or near-new model of your favorite car for a reasonable monthly price. If you’re in a money bind, leasing a car is a great short- to medium-term solution.

Car ownership provides equity and the potential for financial benefit. If you can afford it, the best way to purchase a car is purchase a pre-owned vehicle with cash, directly through the dealership. This avoids interest rates on monthly payments and negates the gap between your financing payments and the car's depreciating value. In some states, there is no sales tax owed on a car. In every state, drivers must pay tax when leasing a vehicle. As an added bonus, car insurance for an owned vehicle tends to be much less expensive than on a leased car.

![]()

Leasing vs Owning a Car: Comparing Control

Lease agreements may limit mileage. Every mile driven in excess of the terms (typically 10,000-15,000 miles) may cost another 15 cents. You can also be overcharged for returning the car in poor condition — as defined by the dealership — or if you request early termination of the contract. Leasing is prudent if you don’t commute daily, or if you only use your vehicle sporadically.

Alternatively, buying your car outright offers a lot more flexibility. You are free to sell the vehicle immediately after purchase — although this is not recommended given potential fees for selling the car before it's completely paid off.

Furthermore, your choices for insurance coverage are much broader. Most leasing companies require you to carry a$100K/$300K bodily injury liability and at least $50K in property damage liability limits, which means a much higher premium than simply getting your state minimum coverage. Be sure to carry bodily injury, property damage, and uninsured and underinsured motorist coverage when applying for a lease. Also consider comprehensive and collision coverages, since the dealership can charge you for any post-crash repairs.

Leasing vs Owning a Car: Comparing Maintenenance Costs

Many leases also include maintenance costs, giving you one less inconvenience to worry about. Maintain a clean exterior and interior and any dealership will be happy to update your lease with a brand new model at the end of your term. So if you're looking to test out the new Tesla, this might be a great option for you.

![]()

When is it better to buy or lease a car?

Consider how you plan to use the vehicle. Drivers who tend to drive a lot (anything more than 12,000 miles a year) might consider buying a car rather than leasing it. Dealers will often charge for any damage to a leased vehicle at the end of the leasing term, and the fees can be expensive.

The most significant drawback to leasing a car is spending money without gaining equity. You're missing a chance to make your money work for you in the long run. Considering today's rising housing prices, and a tight job market, long-term equity may seem out of reach, but owning a significant asset like a home or car can be a significant step toward upward financial mobility.

However, if you’ve got the cash on hand to buy a car outright, absolutely do it. By paying in cash and upfront, you avoid interest rates and finance fees which can add substantial cost. But keep in mind that if the finance rate on your new car is higher than the interest rate you’d earn leaving your money invested, paying the whole bill up front is the still the smartest decision.

![]()

How (bad) credit affects leasing a car

As with any loan, the potential lender will run a credit check to determine if the lease is approved or not. According to LeaseGuide.com, prime credit scores (680-739) will almost always lead to loan approval. Near-prime credit scores (620-679) will usually be approved, but often with a higher interest rate on the loan. Any interest rate above 10% is considered high can be difficult to manage on a monthly basis. Drivers with a credit score of 619 and below are considered sub-prime and may have difficulty getting a car loan. Those with poor credit typically pay higher interest rates.

If you have fair credit, consider buying a used car. At the end of 2017, borrowers with a minimum score of 656 were approved for most used car loans, according to Experian.

How to improve bad credit

If you’re looking at these numbers with some dread, don't panic. There are some simple ways to improve your credit and decrease the interest on your loan.

- ALWAYS make your payments on time. Set up auto-draft on your account with minimum payments so you don’t miss a due date. This is incredibly important: timely payment is the biggest factor used to calculate your credit score.

- Don’t let debt sit on your credit cards. Paying off your balance will boost your credit score.

- Take this next tip with a grain of salt: apply for a new loan. That might seem counterintuitive, but applying for loans actually decreases your credit score. Consider opening a new credit card when you apply for a car loan.

![]()

Leasing a car for Uber or Lyft

Call it a side-hustle, a side-gig, or a second job; the advent of rideshare has proven to be an excellent form of additional income for any generation. Before starting as a rideshare driver, many consider leasing a car solely to use it for their rideshare gig. There’s a smaller down payment and the lease lasts only a few years, which is great if you plan on driving for Uber or Lyft for a short time. Remember, most lease agreements come with mileage restrictions. A lease might be the best option if rideshare driving is not your primary form of income.

A potential drawback is that most dealerships prohibit using a leased car for commercial purposes, which includes ridesharing. The dealerships are concerned with the wear-and-tear that comes with driving a vehicle long-term and places mileage and usage limits in place to prevent this damage. Given the growth of the rideshare economy, many major car companies have worked with Uber and Lyft to provide alternatives. Check out these options if you’re looking to supplement your income by driving a leased car:

- Maven Gig, through General Motors

- HyreCar

- Lyft’s Express Drive program

- Uber’s Xchange program

These additional companies and programs provide rideshare car insurance, avoiding the hassle and expense of insuring a leased vehicle on your personal policy.

In the end, you decide

Buying a car is usually a better long-term financial decision than is leasing a vehicle. The cost of purchasing a car may seem staggering, but the benefit of holding a valuable asset may outweigh the upfront costs. Choosing whether to lease or buy a car is a tricky decision. But with thorough research, a little know-how, and a solid credit score, it’s easier than you may think.