Bodily Injury Liability Insurance

- Carry at least 50/100, ideally 100/300, in bodily injury liability.

- Upgrading to 100/300 from the state minimum costs only $25/mo more on average.

Get the right coverage at the best price—let The Zebra find you savings in minutes.

![]() Why you can trust The Zebra

Why you can trust The Zebra

Ross joined The Zebra as a writer and researcher in 2019. He specialized in writing insurance content to help shoppers make informed decisions.

Ross h…

- 5+ years in the Insurance Industry

Beth joined The Zebra in 2022 as an Associate Content Strategist. A licensed insurance agent, she specializes in creating clear, accessible content t…

- Licensed Insurance Agent — Property and Casualty

- Associate in Insurance (AINS)

- Professional Risk Consultant (PRC)

- Associate in Insurance Services (AIS)

How does bodily injury liability coverage work?

Bodily injury is the part of liability coverage that pays for medical expenses, lost wages, and legal costs of others if you cause an accident that injures someone else. It protects other drivers, passengers, and pedestrians—but not you, your vehicle, or anyone's property.

👉 What this means for you: Be careful when choosing your coverage amount. If you're at fault in an accident and costs exceed your policy limits, you’ll have to pay the rest out of pocket, putting your savings, home, or other assets at risk.

What bodily injury liability covers

-

Medical expenses for injured parties

-

Lost wages for injured parties

-

Legal fees if you're sued

-

Pain and suffering claims

-

Funeral costs for accident victims

-

Your medical bills (covered by health insurance, PIP, or MedPay)

-

Damage to your car (covered by collision coverage)

-

Property damage e.g., fences, buildings (covered by property damage liability insurance)

-

Intentional harm or criminal acts

How much bodily injury coverage do I need?

A good rule of thumb is to match your liability coverage to your net worth—essentially, what’s at risk in a lawsuit. The average bodily injury liability claim was $26,501 in 2022, according to the Insurance Information Institute, part of why we recommend at least 50/100 limits.[1]

However, 100/300 limits or an umbrella policy are usually the best option, especiall if you have significant assets. Even with the average bodily injury claim around $26k, one bad accident can cost far more — especially if multiple people are injured. Higher limits help protect you from those rare but expensive worst-case scenarios.

Choosing the best bodily injury coverage for you

Higher limits offer greater financial security, but the right choice depends on your risk tolerance and financial situation. For the best body injury coverage, (and the most peace of mind) a limit of 100/300/100 is the way to go as it would cover most scenarios. If you have substantial assets, the aforementioned umbrella policy can provide additional coverage beyond standard limits.

| Limits (Per Person/ Per Accident) | Best For* |

|---|---|

| State Minimum (Varies by State) | Not recommended. Leaves you vulnerable to high out-of-pocket expenses. |

| 50/100 | Better protection for budget-conscious drivers. Offers more protection but may not fully cover medical expenses or lawsuits. |

| 100/300 | Best protection for the average driver. Strong financial protection against medical bills and lawsuits for homeowners and those with moderate savings |

| 250/500 | Maximum protection for high-net-worth individuals. Also often the minimum required to have an umbrella policy. |

*These recommendations are general guidelines. The right coverage for you should be based moreso on your net worth and potential financial risk in a lawsuit.

How much bodily injury is full coverage?

Full coverage typically includes 100/300 bodily injury limits—$100,000 per person, $300,000 per accident—or higher. State minimums like 25/50 often aren’t enough to cover serious accidents, leaving you responsible for extra costs. For better protection, consider 250/500 or an umbrella policy.

Do I need umbrella insurance too?

Umbrella insurance is especially important for high-net-worth individuals with more assets at risk, but anyone can face a lawsuit that exceeds their policy limits. Without extra coverage, even middle-class families could be forced to pay out of pocket, drain savings, or take on debt after a serious accident. Here are some quick facts about umbrella insurance:

💰 What it does: Adds $1M+ in extra liability coverage when your auto or home insurance maxes out.

⚖️ What it covers: Medical bills, legal fees, and settlements if you're sued.

📋 Requirements: Many insurers require you to have higher liability limits (e.g., 250/500/100) to get umbrella coverage

My friend’s son—a responsible teen—was one of the drivers in a no-fault accident that seriously injured an elderly passenger. Despite having 250/500/100 liability limits, his family still faced a $750,000 lawsuit and had to cover legal fees themselves. An umbrella policy could have protected them.

Brittany Jinnette — Licensed insurance advisor at The Zebra

Meet the Experts

Have questions about bodily injury liability coverage? Our licensed agents can help you find the right limits and uncover discounts. Call us at 1-888-419-3716 to get expert advice.

Amber Vigil has three years of experience in the insurance industry and joined The Zebra in 2024. As manager, she leads a group of sales agents, ensu…

- Licensed Insurance Agent — Property and Casualty

Blake joined The Zebra in 2021 after a 5-year career at GEICO, where he started as a producer selling auto, property, cycle, RV, and boat policies be…

- Licensed Insurance Agent - Property and Casualty

- 7+ years insurance experience

With a 10-year career in the insurance industry, Jordan brings a wealth of experience in property and casualty insurance. He has experience in both c…

- Licensed Insurance Agent — Property and Casualty

- Licensed Insurance Agent — Life, Health and Variable Annuities

- 10+ insurance experience

How much does increasing bodily injury coverage cost?

Many assume higher coverage is expensive, but the difference is small compared to the risk. Upgrading from the state minimum to 100/300 costs only $25 more per month on average but can save you tens of thousands in a serious accident.[2]

Updating data...

| Bodily Injury Liability Limit | Avg. 6 Mo. Premium | Avg. Monthly Premium |

|---|---|---|

| State minimum | $741 | $123 |

| 100/300 | $880 | $147 |

| 50/100 | $890 | $148 |

Source: The Zebra

The Zebra’s auto insurance data methodology

The Zebra’s Dynamic Insurance Rating Tool for home and auto insurance rates utilizes the latest ZIP code-level rate filings from across the U.S., sourced from Quadrant Information Services and S&P Global. These filings, typically updated annually or biennially by insurers, are verified through Quadrant’s QA process and then integrated into The Zebra’s estimator.

The displayed rates are based on a dynamic home and auto profile designed to reflect the content of the page. This profile is tailored to match specific factors such as age, location, and coverage level, which are adjusted based on the page content to show how these variables can impact premiums.

For a comprehensive understanding, see our detailed methodology.

33% of visitors to this page feel they’re paying too much for car insurance. But skimping on coverage isn’t always the answer.[3] The right insurer and coverage balance can help you save without leaving you financially exposed.

Don’t settle for high rates. Compare quotes and save with The Zebra.

Bodily injury liability limits explained

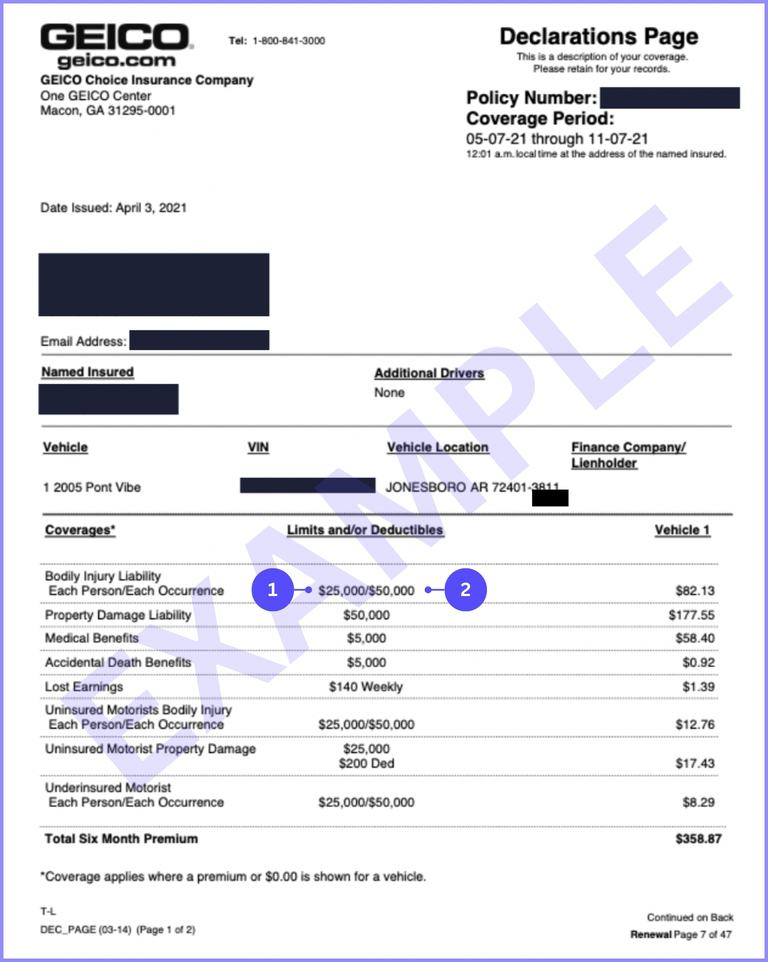

Liability coverage is usually shown as split limits, with separate payout caps for different claims. On your declarations page, it appears as three numbers (e.g., 50/50/50), representing, in order, your per-person limit, per-accident limit, and property damage limit. Some policies, like the sample here, list bodily injury (25/50) and property damage (50) separately.

How bodily injury liability limits work

- Per Person Limit – The maximum your insurer will pay per injured person (e.g. With a $25k per-person limit, your insurer won’t pay more than this for any one individual’s injuries)

- Per Accident Limit – The total amount your insurer will pay for all injured parties combined (e.g. With a $50k per-accident limit, that’s the most your insurer will cover for multiple injuries).

⚠️ Note: No individual can receive more than the per-person limit.

Let’s look at how this might play out if you have 50/100 bodily injury limits:

| Coverage Details | Amount |

|---|---|

| Your Policy Limits | 50/100 |

| Total Medical Bills | $120,000 |

| Your Insurance Pays | $100,000 |

| You Owe | $20,000 |

This example leaves you responsible for $20,000, but the out-of-pocket cost could be much higher. Medical bills from serious accidents can easily reach hundreds of thousands, especially if multiple people are injured or someone requires long-term care. That’s why it’s worth considering higher liability limits if you can afford them. A little extra coverage can go a long way in protecting your finances.

What else does bodily injury liability cover?

You can expect your coverage to pay for the following:

- Medical expenses: The resulting medical bills of those you harmed in the accident.

- Legal fees: If you are taken to court because of your accident, this coverage can go toward covering the cost of your legal defense.

- Lost wages: If the injuries you cause to another person while behind the wheel result in someone not being able to work, your bodily injury coverage could help cover wages lost.

- Funeral costs: If you cause an accident that results in fatalities, bodily injury liability can help cover funeral expenses.

- Pain and suffering: While it can be hard to show the exact emotional impact that an accident has caused, liability insurance will cover the emotional distress that you cause to another person. Some states may limit the amount allowed for such a claim.

What are the bodily injury liability limits in each state?

Each state (except Florida) sets minimum bodily injury liability limits that drivers must carry. However, state minimums are often too low to fully cover medical bills and lawsuits after an accident. The most common state minimum is 25/50/25. We recommend at least 50/100/50 for better protection, while 100/300/100 is the best choice for covering most accident scenarios.

Even in no-fault states with PIP, liability coverage is still essential. You still need at least 50/100/50—ideally 100/300/100—to fully protect yourself. Why?

✔ PIP Has Limits – It only covers medical bills and lost wages up to a set amount—not pain, suffering, or severe injury claims

⚠️ You Can Still Be Sued – If injuries exceed PIP limits or meet lawsuit thresholds, you’re financially responsible.

Exceptions to carrying bodily injury liability

Most states require bodily injury liability, but there are a couple of exceptions.

In some cases, your state may allow you an exemption if you can prove that you have sufficient funds to cover any damage that you may cause. This is often done by posting a bond with the state that is typically higher than the insurance limits required.

Instead of separate limits for bodily injury and property damage, some states let you combine them into one overall coverage amount. This gives you more flexibility—if you injure someone, you can use more of your total coverage for their medical bills instead of being limited by a per-person cap.

⚠️ WARNING: Even if your state offers alternatives, going without can be risky. If costs exceed your bond or combined limit, you’re responsible for the rest. For most drivers, having high bodily injury liability limits is the smartest option.

Considerations

In general, it’s important to keep your bodily injury liability limits as high as you can reasonably afford. If you are concerned about the added costs of increasing your coverage, it may be time to compare rates and weigh your options.

The Zebra can help you find low-cost insurance quotes from top insurers, giving you the chance to receive quotes from multiple insurers and find an auto policy that is right for you.

Weigh your options and get the best value from your next insurance policy.

Bodily injury liability FAQs

-

Facts + Statistics: Auto insurance. The Insurance Information Institute.

Facts + Statistics: Auto insurance. The Insurance Information Institute.

-

Data Methodology. The Zebra’s Dynamic Insurance Rating Tool

Data Methodology. The Zebra’s Dynamic Insurance Rating Tool

-

Anonymized User Surveys. The Zebra

Anonymized User Surveys. The Zebra

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.