Key statistics + insights

Every year, The Zebra releases an analysis of more than 73 million unique auto insurance rates. Then, our in-house research team breaks down the pricing data from every zip code in the United States and gathers the most interesting findings.

The following statistics reflect the current price of car insurance and the overall national increase in car insurance premiums.

- $1,759 is the average car insurance premium in the United States.

- Since 2011, rates have skyrocketed by 29.6% nationally. The rate of increase varies by individual state and city.

- Average annual rates now exceed $6,000 in some American cities, more than three times the national average.

For the full analysis, please refer to our most recent Insurance Outlook for 2023.

Compare insurance rates online for free today.

Car insurance statistics breakdown

- Auto insurance statistics by state

- Auto insurance premiums by vehichle type

- Auto insurance statistics by demographics

- Auto insurance and technology statistics

- Does your driving record affect your car insurance rates?

- Trends in auto insurance policies

- Telemetics' impact on car insurance rates

- Bundling discounts

Auto insurance statistics by state

- In 2023, Michigan has the largest average auto insurance rates at $211 a month.

- In 2019, South Dakota saw the biggest year-over-year rate increase at 22% while Texas saw the biggest rate decrease: -20%.

- Overall in 2019, Michigan remained the state where car insurance is most expensive, with an average cost of $3,096. The capital of Michigan, Detroit, continues to be the most expensive city in the United States with premiums more than four times the national average ($6,208).

- The least expensive state in the nation is Maine, with annual average premiums costing $935.

- Winston-Salem, North Carolina, was the major city with the cheapest rates: $847.

- The New England region is the cheapest region for car insurance in the US, with average costs of $1,305 a year.

- The Far West region is the most expensive region for car insurance in the US, with an average rate of $1,665 a year.

- Only seven states have enjoyed rate decreases since 2011, while 44 states — including Washington D.C. — witnessed significant increases (up to 86%).

10 most expensive states for car insurance in 2023

| State | Average Monthly Premium |

| Michigan | $211 |

| Florida | $194 |

| Louisiana | $192 |

| Rhode Island | $156 |

| Kentucky | $154 |

| California | $152 |

| Nevada | $145 |

| Arkansas | $142 |

| Colorado | $142 |

| Missouri | $141 |

10 most inexpensive states for car insurance in 2023

| State | Average Monthly Premium |

| Ohio | $77 |

| New Hampshire | $80 |

| North Carolina | $84 |

| Virginia | $86 |

| Vermont | $88 |

| Hawaii | $90 |

| Wisconsin | $90 |

| Maine | $92 |

| Iowa | $96 |

| Indiana | $99 |

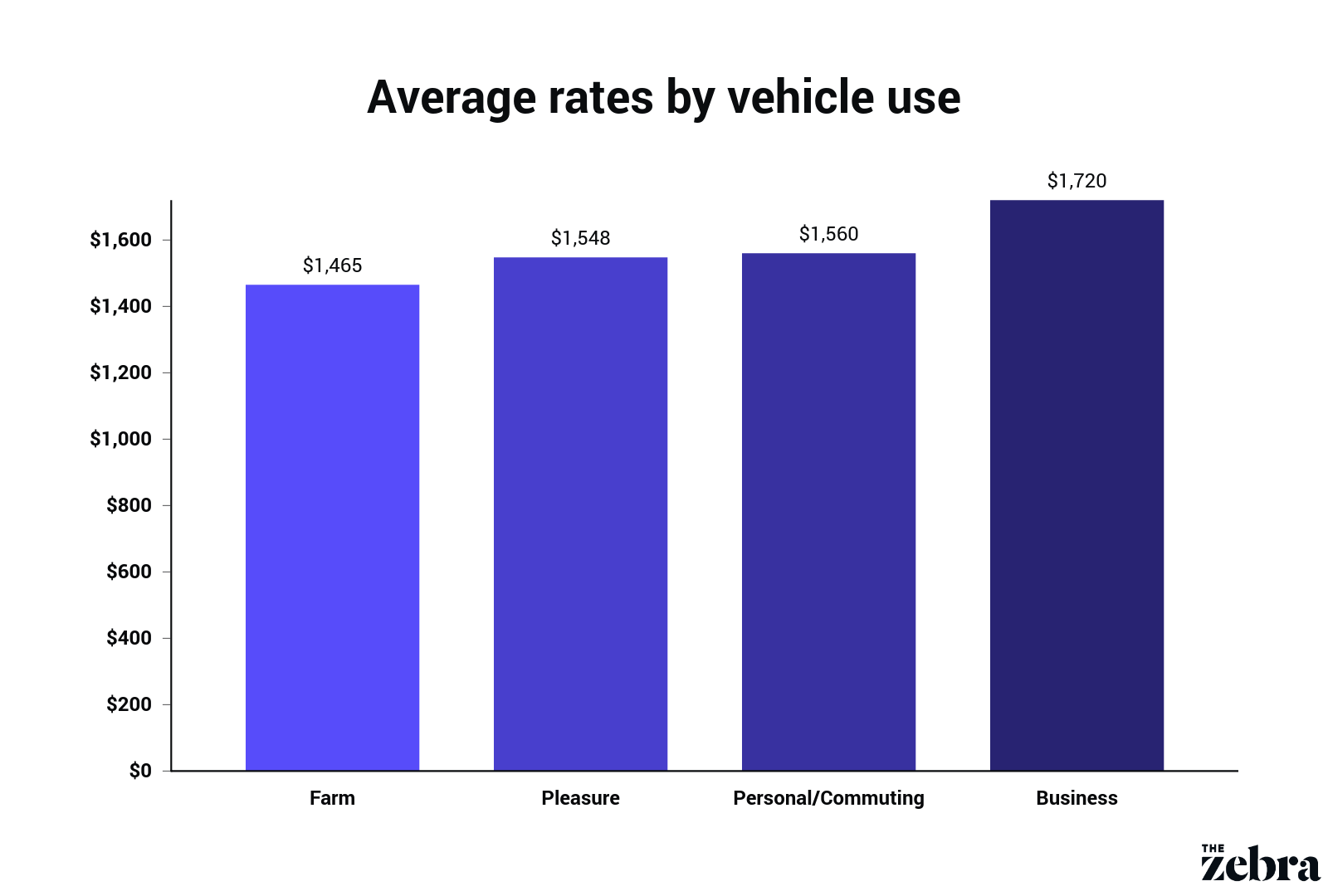

Auto insurance premiums by vehicle

- In 2023, the most expensive car to insure is the Maserati Quattroporte, which costs an average of $419 per month, 239% more than the national average for auto insurance.

- By percentage of MSRP, Nissan was the most expensive vehicle brand to ensure, at 8.7%.

- By percentage of MSRP, Porsche was the least expensive brand to insure (3.6%).

- Vans were the cheapest car type to insure with annual premiums totaling $1,688.

- Sedans were the most expensive vehicle type to insure, with average costs coming to $2,275 per year.

- Eco-friendly buyers beware: green/hybrid cars are some of the most expensive models to insure due to the cost of repairs and replacement — $2,110 to insure a year, on average.

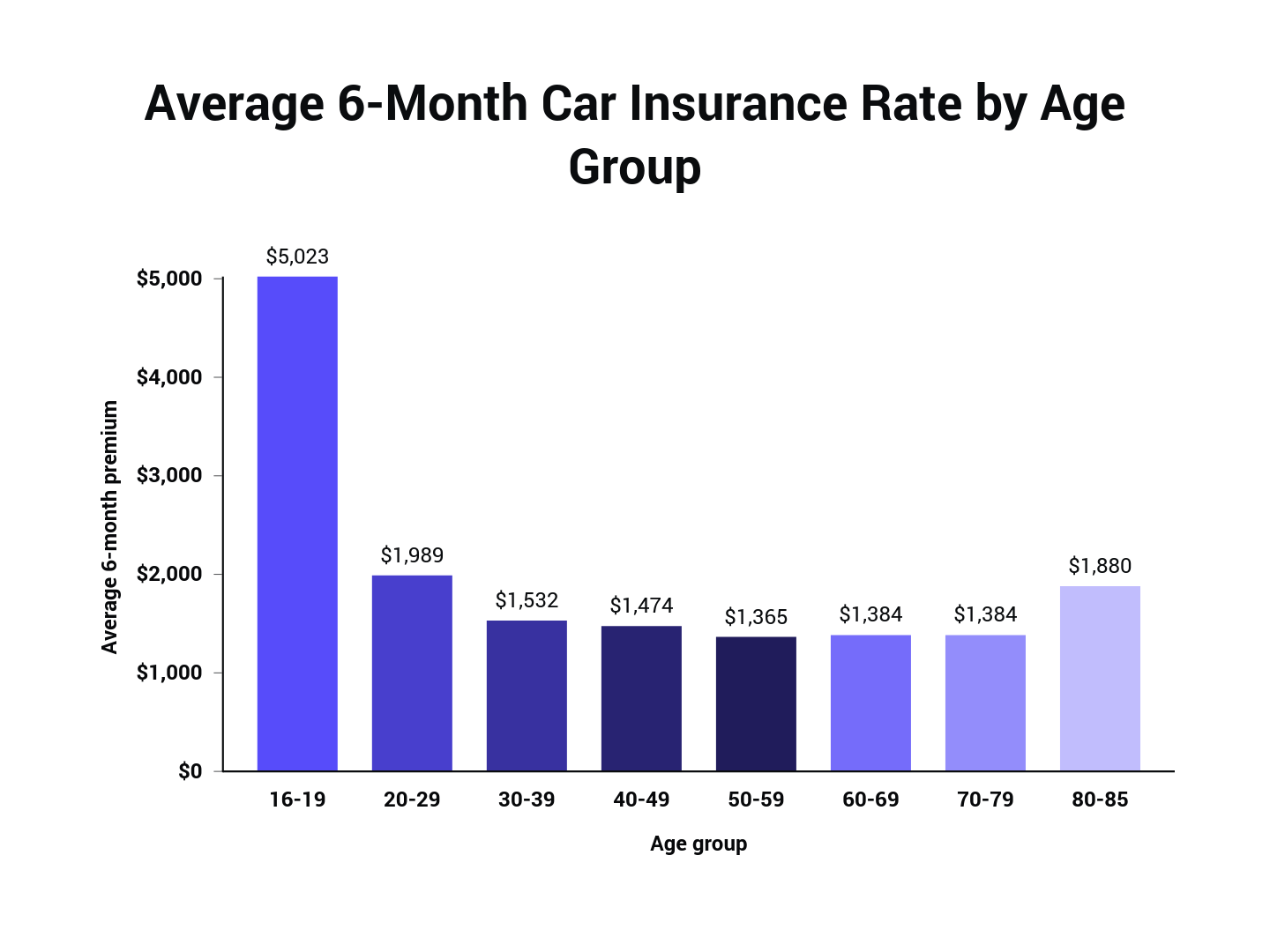

Car insurance premiums demographic statistics

- Nationally, drivers aged 55 and up experience the cheapest rates.

- A 16-year-old driver with a policy of their own would pay, on average, $6,600 per year for car insurance — more than three times the average for drivers ages 23 to 85.

- On average, the difference between what women and men pay for car insurance is insignificant, with women paying less than 1% more than men.

- However, this average also varies by state: women in Louisiana pay 5% more than men, while men in Wyoming pay 3.7% more than women.

- Motorists with poor credit pay 114% ($1,546) more for car insurance than drivers who have exceptional credit (a credit score of 750 and above).

- Getting married can reduce your car insurance rates by about 6%, saving about $98 per year. Only a handful of states, including Montana, Massachusetts, and Hawaii, don’t allow insurers to consider marital status in determining rates.

- There are reasons to get that GED: drivers with no high school diploma pay only about 3.6% ($57) more per year than drivers who have a Ph.D.

- Being employed full-time can save you 1.3% ($21) on car insurance.

- Active duty military personnel get an average discount of 2.6% ($40) over civilians.

Auto insurance and technology statistics

Many new car models are outfitted with advanced technology that enhances safety and prevents theft. However, this technology also increases the cost of vehicle repairs or replacement, so it won’t save you much on car insurance.

- Implementing electronic stability control (ESC) in your vehicle will lower auto insurance premiums by $8 a year on average.

- All other safety devices (including a blind-spot warning device, lane departure warning, and night vision) offer essentially no additional savings in auto insurance premiums.

- There is no anti-theft device out there that saves more than 1% on average auto insurance costs.

Car insurance violations trends

Your driving record is one of the most significant factors in determining your car insurance rates.

- A citation for leaving the scene of an accident, i.e., a hit and run, will affect your auto insurance premiums more than any other violation. This is true for every year from 2011-2019.

- Getting caught texting or otherwise using your phone while driving will raise your insurance rate by an average of 23% ($356) — and in some states by more than 63%.

- Based on the average American driving about 12,000 miles per year, drivers can save about 6% if they reduce their mileage from 15,000 per year to less than 7,500 miles per year.

Average increased cost of auto insurance by accident/violation

| Year | 2015 | 2016 | 2017 | 2018 | 2019 |

| Cell Phone Violation | $84 | $184 | $238 | $321 | $355 |

| Texting while Driving | $84 | $185 | $240 | $323 | $357 |

Auto insurance policy trends and analysis in the insurance market

Car insurance coverage can be divided into two primary categories: liability and bodily injury (together forming full coverage auto insurance). Liability coverage protects other drivers and their property from the physical damage you cause. Physical coverage, i.e., collision and comprehensive, protect the integrity of your vehicle from property damage.

- Motorists with usage-based insurance (UBI) policies save about 3% on their car insurance premiums.

- Raising your deductible from $500 to $1,000 saves an average of 13% on your total insurance rate for the year with your insurance provider.

- A driver who maintained 100/300 liability coverage for five years would save 15%.

- If you have insurance for five years or more, you can save 9% on your premiums. The history of car insurance is more important than staying with a specific car insurance company.

- Maintaining a state minimum liability cost offers the least amount of protection for the lowest price.

- Adding rideshare coverage if you use your own vehicle to drive for Lyft or Uber can raise your rates by 15%.

- In order to save about $186 or 12% in savings on your rates, be sure to use these discounts:

- Pay online

- Payment in full

- Advanced payment

Telematics' impact on car insurance rates

| Telematics status | Average Annual Premium |

| Telematics - No | $1,548 |

| Telematics - Yes | $1,502 |

Car insurance discounts via bundling

Taking out two separate policies from the same insurance company is known as bundling.

- When you bundle coverage for your apartment, house, or condo with coverage for your car, you can save 5-10% on car insurance.

- Nationally, renters pay slightly more for car insurance than home or condo owners (regardless of whether or not they choose to bundle policies). In some states, renters pay as much as 7.3% more than homeowners for car insurance.

Frequently Asked Questions about the car insurance industry

Q: How much is the car insurance industry worth?

In 2020, the estimated revenue for the automobile insurance industry is $288.4 billion.

Q: How big is the car insurance industry?

There are more than 500 car insurance providers in the U.S., each with their own prices and policies. There are even more companies within the industry providing additional services such as rate comparisons.

Q: What are the current trends in the insurance industry?

The insurance industry is being revolutionized by technology. New technology like automated driving is being introduced to consumers, and insurance companies are having to address it within their offerings and policies. There are also many insuretech companies being created to save more time and money for consumers.

Q: Is the insurance industry growing?

As an industry, insurance has always been slow-growing. However, with many insuretech companies disrupting the industry, there has been a pivot in where the industry is headed within the next five to ten years.

Methodology

The auto insurance rates displayed in our articles are based on the 2019 results of The Zebra’s comprehensive car insurance pricing analysis. In our analysis of all US ZIP codes — including Washington D.C. — our user profile consisted of a 30-year-old single male driving a 2013 Honda Accord. To generate pricing specific to particular rating factors, we altered the driving profile based on the common pricing factors utilized by top car insurance companies. These factors include, but are not limited to, credit score, coverage level, and driving record.

Our homeowner's results are compiled from the same ZIP code but a 45-year-old homeowner with a $200,000 and $400,000 dwelling value. Our renter's insurance results are determined from a 30-year-old male with $25,000 or $50,000 of personal property contents. Each of these profiles uses the same ZIP codes as our auto insurance rates.

Stay in touch and subscribe!

Get advice, insights and tips from our newsletter.