Homebuying FOMO in America

Homeownership continues to be the cornerstone of the American dream, but the journey to achieving it isn’t getting any easier. The pandemic, shifts toward remote work and historically low mortgage rates have caused an influx of home buyers, resulting in stiff competition in housing markets across the country. When this competition is combined with declining home inventories, the real estate industry reports that surges in home sales are driven by home-buying FOMO, or the fear of missing out.[1][2]

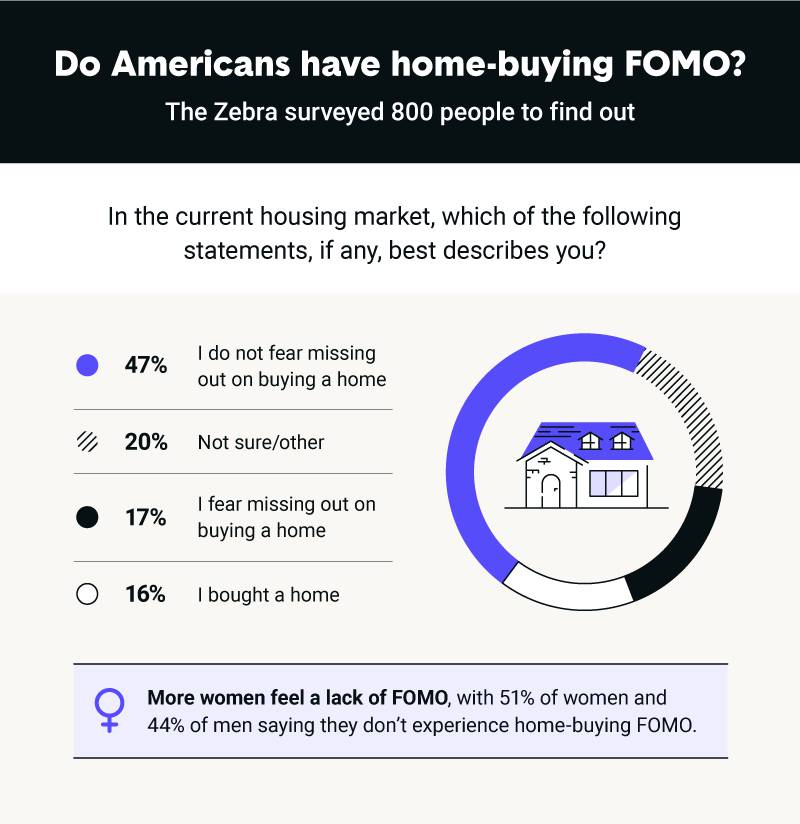

To see the extent of home-buying FOMO across the country, The Zebra surveyed 800 people about their home-buying intentions, what pressures affected their decision to buy in today’s hot housing market and whether they feared missing out on buying a home. Below are some notable findings.

Key findings:

- 47% of Americans claim they don’t fear missing out on buying a home in today’s competitive market.

- On the other hand, 17% of Americans do fear missing out on buying a home during the current housing market.

- One in two Americans are satisfied with their home purchases.

- A surprising 14% of Americans don’t plan on becoming homeowners.

- The financial ability to buy is the biggest consideration Americans have when deciding to buy a home.

Although home-buying FOMO may be a visceral experience, it shouldn’t be the only reason you decide to buy a home. Below, we discuss the pros and cons of owning a house to see if it’s right for you. If you did make a home purchase in today’s competitive market, make sure you take steps to protect your home for the long run.