![]() Why you can trust The Zebra

Why you can trust The Zebra

Kristine joined The Zebra in 2019 as an in-house content researcher and writer, with a property and casualty insurance license. Before joining The Ze…

- Licensed Insurance Agent — Property and Casualty

- 6+ years of Experience in the Insurance Industry

Ross joined The Zebra as a writer and researcher in 2019. He specialized in writing insurance content to help shoppers make informed decisions.

Ross h…

- 5+ years in the Insurance Industry

What is a high-risk life insurance policy?

High-risk life insurance is coverage for people who are risky to insure. Lifestyle factors like life-threatening occupations, hobbies, habits or travel can all contribute to what makes a person “high risk” to a life insurance company. Additionally, if you have chronic health conditions or illnesses, you’re also considered high risk.

People of all walks of life use life insurance as a safety net for their families in case the unexpected happens and they’re no longer around to provide for them. When applying for life insurance, many factors will influence your coverage options and how much you’ll end up paying for premiums. While most people in good health can easily purchase an affordable policy, the process can be more difficult if you’re considered “high risk.”

To help you figure out whether you need high-risk life insurance, check out this guide to learn about the lifestyle and health factors that contribute to being determined as high risk. If you already know you’re considered high risk, jump to our infographics that outline essential safety tips for anyone with a high-risk job or hobby.

Factors that determine life insurance risk

Generally, factors that affect your health and life expectancy will affect your life insurance risk. The higher the risk you are, the higher your policy premiums will be. Read about the most common risk factors below.

High medical risk

If you plan to purchase life insurance, you’ll either need to undergo a full medical exam or answer questions about your health and medical history. Companies will focus on chronic health conditions and terminal illnesses that may shorten your life expectancy to classify high medical risk. Your risk can be determined based on whether you currently have a condition or if you have a family history of it. The following are some medical conditions that are considered high risk.

- ALS or Lou Gehrig’s disease

- Cancer

- Chronic obstructive coronary disease (COPD)

- Congestive heart failure

- Dementia

- Heart disease

- High cholesterol

- HIV/AIDS

- Kidney disease

- Long COVID

- Organ transplants

- Stroke

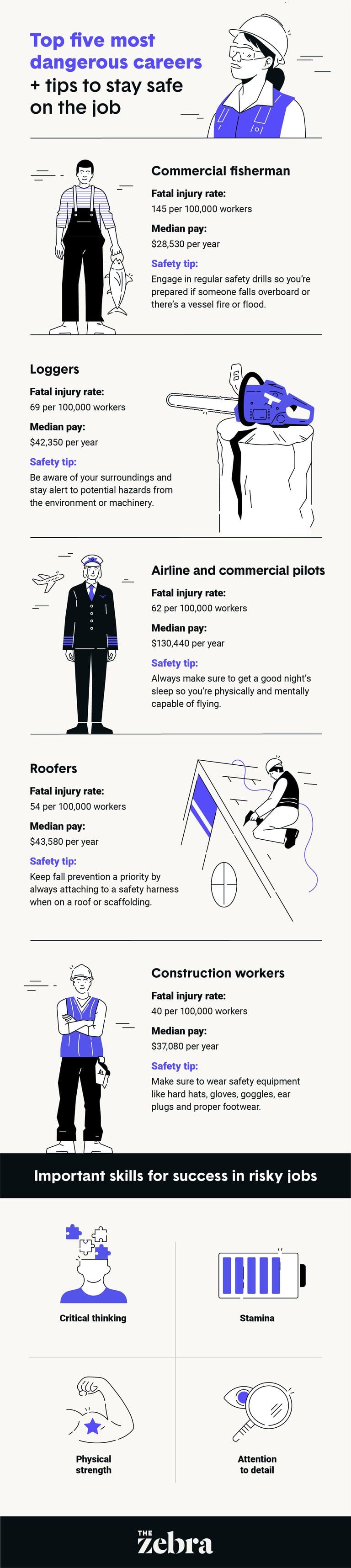

High-risk occupations

When it comes to figuring out whether you’re in a high-risk profession, it’s important to know that life insurance companies use mortality rates to classify jobs. Occupations with high mortality rates like fishing and hunting workers, loggers, aircraft pilots and engineers and roofers are all considered high risk. Insurance companies will classify each profession’s risk based on mortality rate, so check out some examples of careers with high fatality rates below.

- Fishing and hunting workers: 145 fatal injuries per 100,000 full-time workers

- Logging workers: 69 fatal injuries per 100,000 full-time workers

- Aircraft pilots and engineers: 62 fatal injuries per 100,000 full-time workers

- Roofers: 54 fatal injuries per 100,000 full-time workers

- Construction workers: 40 fatal injuries per 100,000 full-time workers

High-risk habits

Certain lifestyle habits also contribute to whether you’re considered high risk or not. Habits like heavy alcohol consumption or tobacco use can have adverse effects on your health and will in turn, limit your coverage options and increase your premiums. Additionally, if you engage in risky habits excessively, you may even be denied coverage altogether. Find some common high-risk habits outlined below.

- Chewing tobacco

- Consuming non-prescription drugs

- Excessive alcohol consumption

- Smoking cigars or cigarettes

- Vaping

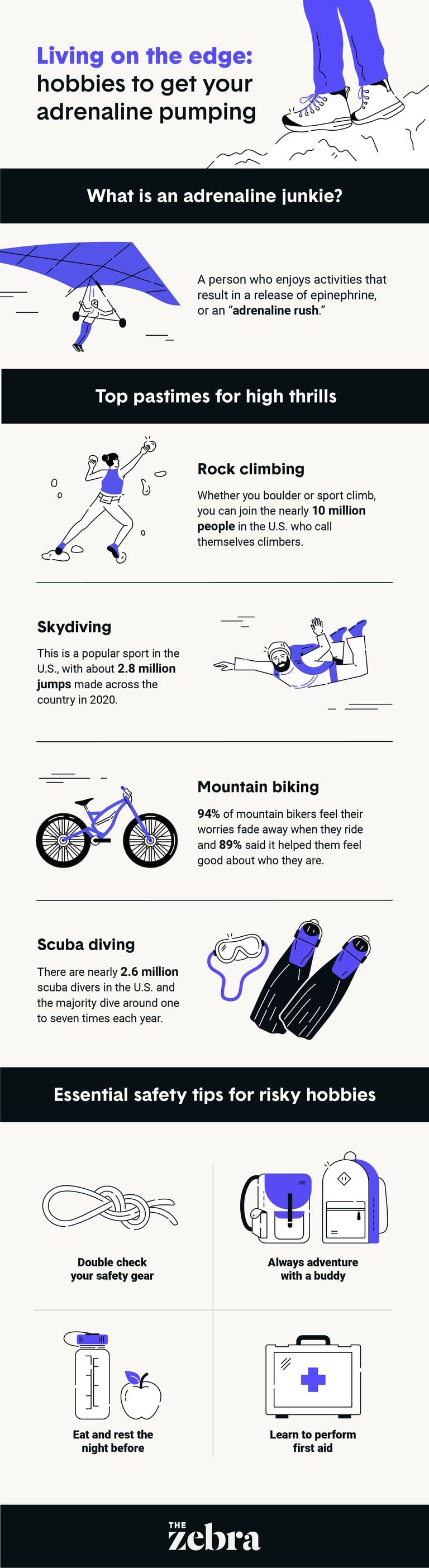

High-risk hobbies

Believe it or not, your hobbies can also determine whether you’re considered high risk to life insurance underwriters. Any hobby has the potential to pose certain risks to your health. For example, relatively safe hobbies like baking or gardening may result in minor scrapes and burns, but these aren’t the kinds of hobbies that affect your life insurance.

Adrenaline-pumping activities like bungee jumping and scuba diving can be dangerous and potentially life-threatening. It’s these types of hobbies that are considered high risk. If you’re considering doing something risky like skydiving just once in your life, most companies won’t classify you as a high-risk individual. However, if you participate in risky hobbies frequently, you’d be considered high risk to insurers and will most likely pay more for coverage. See the list below to see if any of your favorite pastimes are high risk.

- Bungee jumping

- Car or motorcycle racing

- Hang gliding

- Mountaineering

- Parachuting

- Rock climbing

- Scuba diving

- Skydiving

Can you get insurance if you are high-risk?

Despite being considered high risk by a life insurance company, it’s still possible to buy life insurance. Because certain lifestyles and health conditions are considered riskier to insure, high-risk life insurance policies are often more expensive to purchase and may be limited in coverage.

Tips for obtaining affordable high-risk life insurance

Even if you’re considered high risk by life insurance companies, there are still ways to make sure you get the best premiums possible. Read on for three tips that will help you find an affordable high-risk life insurance policy.

Compare companies and policies

Although it’s risky for insurance companies to cover high-risk individuals, there’s enough competition in the industry to still find competitive rates. Compare plans from various companies or agents to find the coverage and the premium that works best for you.

Different companies also have varying underwriting standards and conditions for coverage. If one company has a premium that is too high for you or even denies you coverage, another may be more affordable or more lenient. Remember to use The Zebra to get personalized life insurance quotes from the comfort of your own home.

Improve your health

Because your life expectancy is a factor that’s used to determine your risk, improving your health can go a long way toward decreasing what you pay for life insurance. If you have a manageable health condition, it’s important to work with your doctor or a specialized medical professional to create an action plan toward better health. For example, if you have high cholesterol, doing whatever you can to lower your cholesterol through exercise, diet or medication will not only improve your life expectancy but also help reduce your premiums.

Consider a lifestyle change

If your lifestyle is the reason you need high-risk life insurance, it may be time to consider a change. For those that are willing to stop risky habits, switch to a safer job or stay away from dangerous hobbies, you’ll have a much easier time obtaining affordable life insurance.

If you’re not ready to give up your thrill-seeking ways or drop high-risk habits, reducing the frequency of them can also help lower your premiums. Most companies will provide better rates for someone who only scuba dives a few times a year or enjoys a cigar or two than someone who engages in these activities more frequently.

FAQs about high-risk life insurance

By now you’re probably able to figure out if you need high-risk life insurance based on your occupation, habits, hobbies and medical history. If you’re looking for more answers, check out a couple of frequently asked questions below.

How are rates determined for high-risk life insurance?

After applying for life insurance, your application will be given a health rating and risk level. These two things are influenced by questions you were asked about your health and lifestyle and a medical exam if you took one. The premium you pay is based on the rating you were given by the life insurance company. You can reference a typical rating scale below.

Life insurance risk ratings |

|

|

Preferred select |

|

|

Preferred |

|

|

Standard plus |

|

|

Standard |

|

|

Preferred smoker |

|

|

Standard smoker |

|

|

Table rating |

|

What is a table rating?

High-risk individuals are given a table rating. Applicants with table ratings are assigned a letter (A-P) or a number (1-16) that determines how much more will be paid. The letter or number refers to a percentage above the standard premium, and each subsequent rating on the table increases by 25%. If someone is rated a 1 or A, they would pay 25% more than the standard premium. Someone rated a 5 or E would pay 125% more than the standard premium. Find all 16 ratings and their corresponding percentages below.

Table rating percentage increases |

||

|

1 |

A |

25% |

|

2 |

B |

50% |

|

3 |

C |

75% |

|

4 |

D |

100% |

|

5 |

E |

125% |

|

6 |

F |

150% |

|

7 |

G |

175% |

|

8 |

H |

200% |

|

9 |

I |

225% |

|

10 |

J |

250% |

|

11 |

K |

275% |

|

12 |

L |

300% |

|

13 |

M |

325% |

|

14 |

N |

350% |

|

15 |

O |

375% |

|

16 |

P |

400% |

What is a group insurance plan?

Group insurance plans are often offered by employers of those in high-risk jobs. Employees may have difficulty finding coverage on their own due to the nature of their work, so employers will offer a certain amount of life insurance. Group plans tend to have basic coverage and generally have restrictions that come in the form of maximum coverage limits. If your work gives you basic coverage through a group plan, it may be in your best interest to pick up a supplemental plan through your employer or another company.

Obtaining life insurance is important if you want to take care of your family in case you pass prematurely. If you have a great medical history and lead a lifestyle with relatively little risk, it can be easy to get good coverage. For those who live life on the edge or happen to have a more complex medical record, finding affordable coverage may be tougher. If you’re considered high risk, use this guide to learn more and try out our tips to help you purchase an affordable life insurance policy.

Sources: Bureau of Labor Statistics 1 2 | Medical News Today | Statista | United States Parachute Association | Frontiers in Psychology | Sports & Fitness Industry Association |

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.