Credit and car insurance

How does your credit score affect the price of your car insurance rates? How does that vary by state?

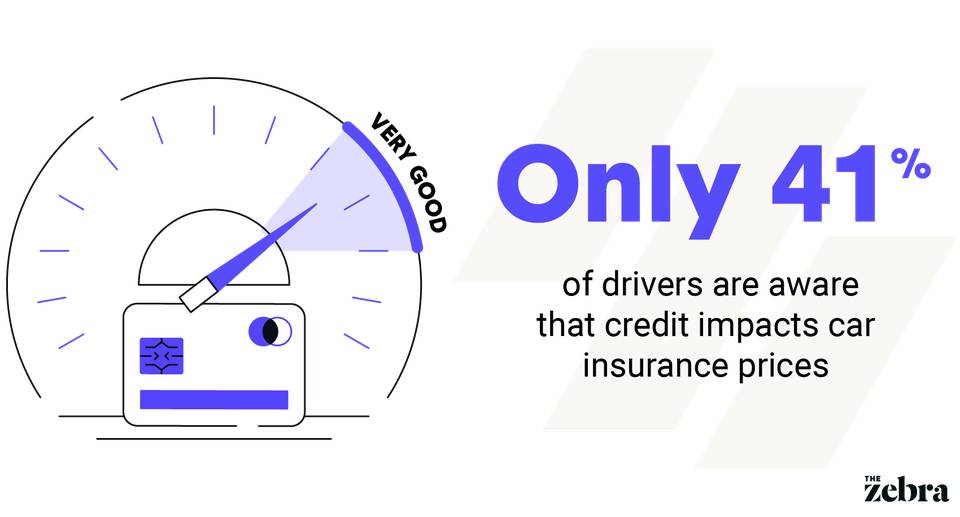

Most consumers know that credit plays a big role in their finances, whether they’re applying for a credit card or considering a car or home loan.

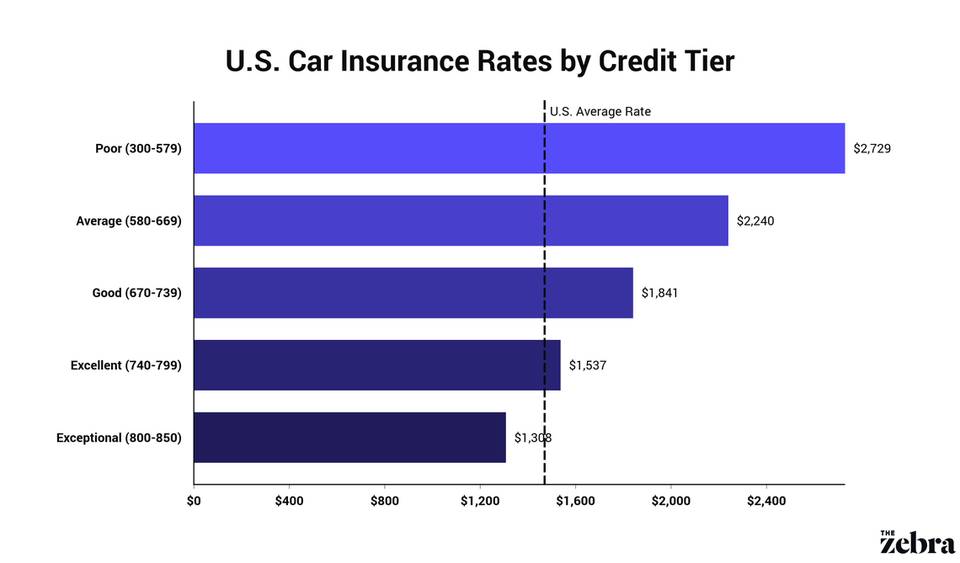

What most consumers don’t realize is that, in nearly every state, credit also has a huge impact on what they pay for car insurance. In fact, dropping just one credit tier can increase a driver’s car insurance premium an average of 17% or $355 per year.

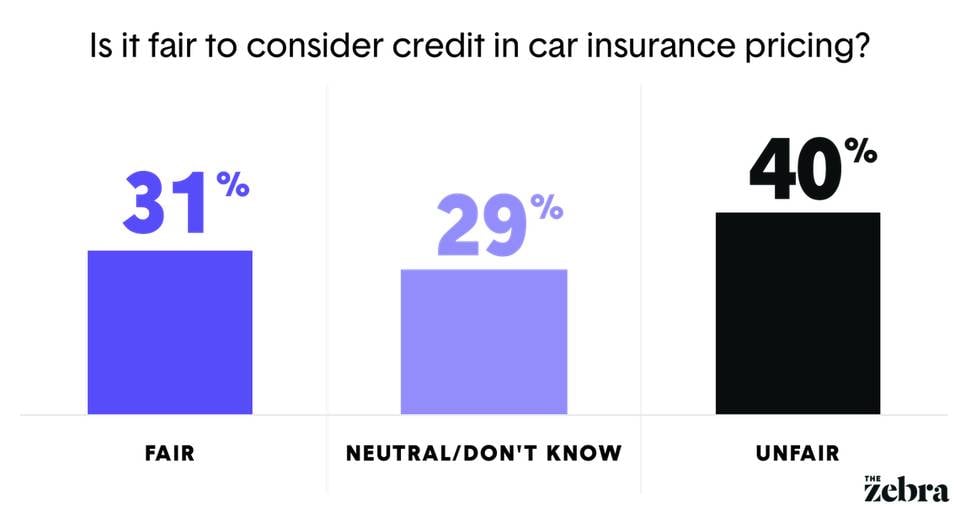

If this sounds concerning, you’re not alone. Several states (California, Maryland, Michigan, Massachusetts and Hawaii) ban or limit insurers' use of credit in car insurance pricing.[1] Other states have certain circumstances where credit can be used (Utah, Nevada, Oregon, Washington, North Carolina), but many state legislatures continue to debate the use of credit.[2] It's ultimately up to the state to decide how and when this information can be applied to insurance, so we suggest checking your state's Department of Insurance website for specific details.

Just how big a credit's impact on insurance rates varies by insurer and location. Here, we review the impacts in each state and share what consumers can do to ensure they’re getting the best rate.