About

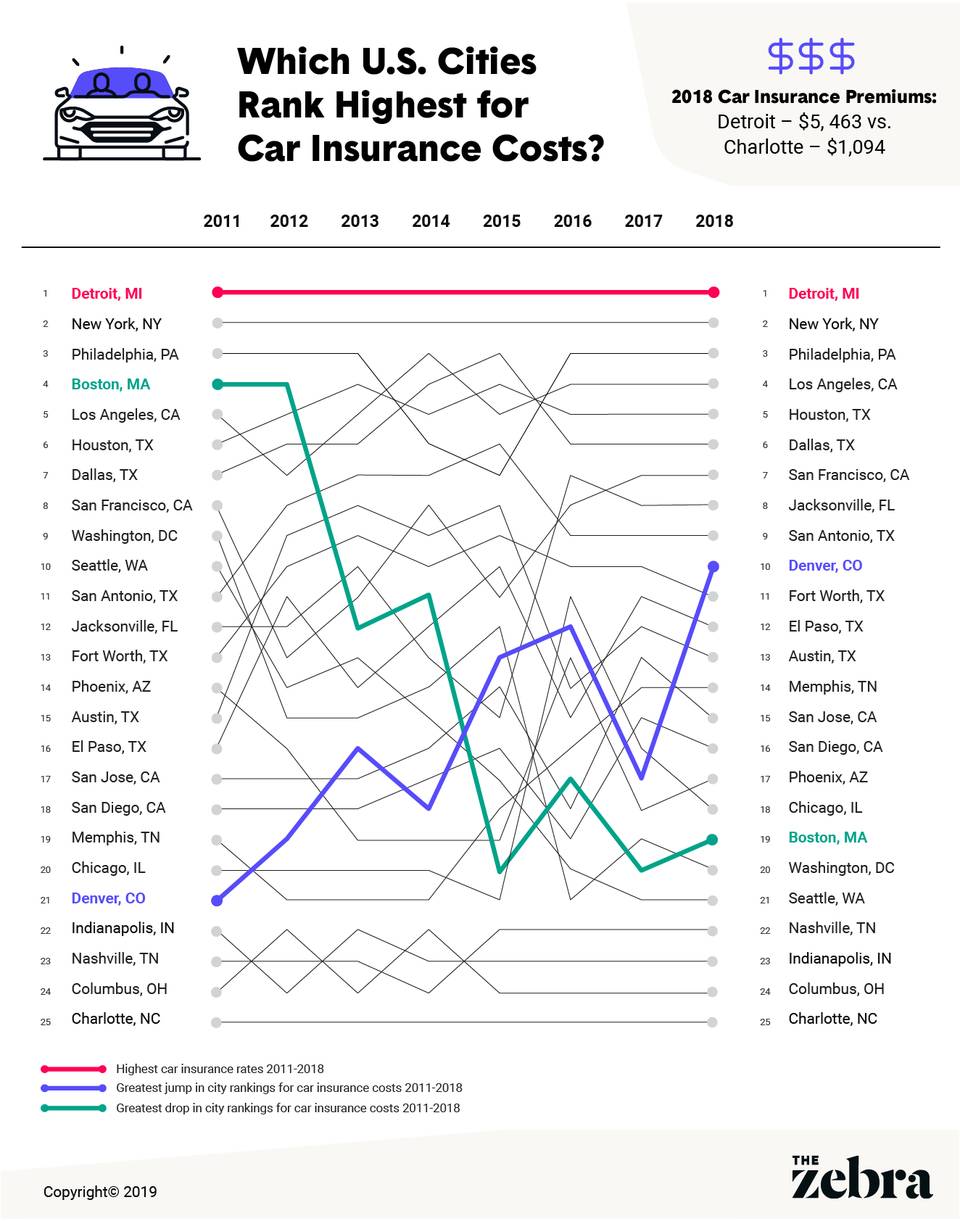

Car insurance costs have steadily increased in the U.S. in the past decade, but no state has felt the impact quite like Michigan. Drivers there pay the highest car insurance rates in the country.

But that could change following Michigan’s passage of sweeping car insurance reform, which went into effect July 2, 2020. The new law makes major changes and, significantly, it eliminates the state’s requirement that all drivers buy unlimited, lifetime medical coverage for car accident injuries.

Here we take a look at the changes and the options now available to Michigan drivers.

This report explores:

- Why Michigan Has the Highest Car Insurance Rates in the Country

- Car Insurance Changes — and New Coverage Options — for all Michigan Drivers

- What Michigan Drivers Can Do to Make Sure They’re Getting the Best Rate