Car Insurance with Telematics

Telematics car insurance, which tracks driving habits to potentially lower rates, can be worth it for safe, low-mileage drivers looking to save money.

![]() Why you can trust The Zebra

Why you can trust The Zebra

Ross joined The Zebra as a writer and researcher in 2019. He specialized in writing insurance content to help shoppers make informed decisions.

Ross h…

- 5+ years in the Insurance Industry

Beth joined The Zebra in 2022 as an Associate Content Strategist. A licensed insurance agent, she specializes in creating clear, accessible content t…

- Licensed Insurance Agent — Property and Casualty

- Associate in Insurance (AINS)

- Professional Risk Consultant (PRC)

- Associate in Insurance Services (AIS)

What is telematics car insurance?

Also known as usage-based insurance (UBI), telematics-powered auto insurance uses an app, plug-in device, or built-in vehicle device to track things like your speed, mileage, total driving time and other driving habits. This data helps determine your premium. And with the global telematics insurance market projected to grow from $5.89 billion in 2025 to $19.23 billion by 2032, this data-driven model is only becoming more common.[1]

👉 What this means for you: If you're a safe driver — especially one who doesn’t spend much time on the road — telematics could help lower your rate.

The best telematics car insurance companies

The Zebra's Choice: State Farm Drive Safe & Save

Drive Safe & Save offers the best value when balancing cost ($101 per month)[2] availability, and app usability.

Cheapest: USAA SafePilot

USAA's SafePilot app had the lowest average rate at $90 per month (but it's also highly rated!).

Best risk-free option: American Family KnowYourDrive

Never raises your rate for poor driving, but instead gives you a discount at renewal.

Usage-based insurance vs pay-per-mile: What's the difference

Telematics is the technology in your car or on your phone that car insurance companies use to track your driving behavior. Usage-based insurance (UBI) is the type of insurance that uses that technology. There are a few ways insurers use telematics to price policies. Here’s a breakdown of the most common types — what they track, who they’re generally best for, and real-world examples.

| Type | What It Is / Best For | Examples |

|---|---|---|

| Pay-Per-Mile | Pay-per-mile charges based on how many miles you drive. Great for low-mileage drivers. | Metromile, Mile Auto, Nationwide SmartMiles |

| Useage-Based Insurance | Useage-based insurance uses driving behavior (speed, braking, etc.) and sometimes also mileage to set your rate. Good for safe daily drivers. | Progressive Snapshot, GEICO DriveEasy, Allstate Drivewise |

| On-Demand/Pay-as-You-Go | On-demand (aka pay-as-you-go insurance) allows you to turn coverage on and off as needed. Works well for those who want on-demand insurance and can stay on top of activating and deactivating it as their driving needs change. | Hugo |

How telematics works

Telematics insurance works by tracking your driving, generating a score, and adjusting your premium based on that score. The steps are similar across most programs, though the technology used can vary.

-

You sign up and set up — either by downloading an app, plugging in a device, or activating your car’s built-in system.

-

Your driving is tracked — including behaviors like speed, braking, mileage, phone use, and time of day, usually for 60-90 days.

-

You receive a driving score — usually visible in the app, which reflects how safe (or risky) your habits are.

-

Your premium adjusts — some programs apply discounts only, while others can increase your rate for risky driving. Rate changes may happen monthly or at renewal.

How it differs by tech

📱 App-Based Tracking. Your phone tracks trips using GPS and sensors. It's easy to set up, but you may need to reclassify shared trips or deal with occasional app glitches.

🔌 Plug-In Device. A small device connects to your car’s internal system to track data. It’s more accurate and less hands-on but only works with vehicles that support it.

🚘 Connected Car. Built-in systems (like OnStar or Blue Link) send data directly to your insurer. It’s fully automated, but only available in some 2020 or newer vehicles and from a few insurers (primarily State Farm).

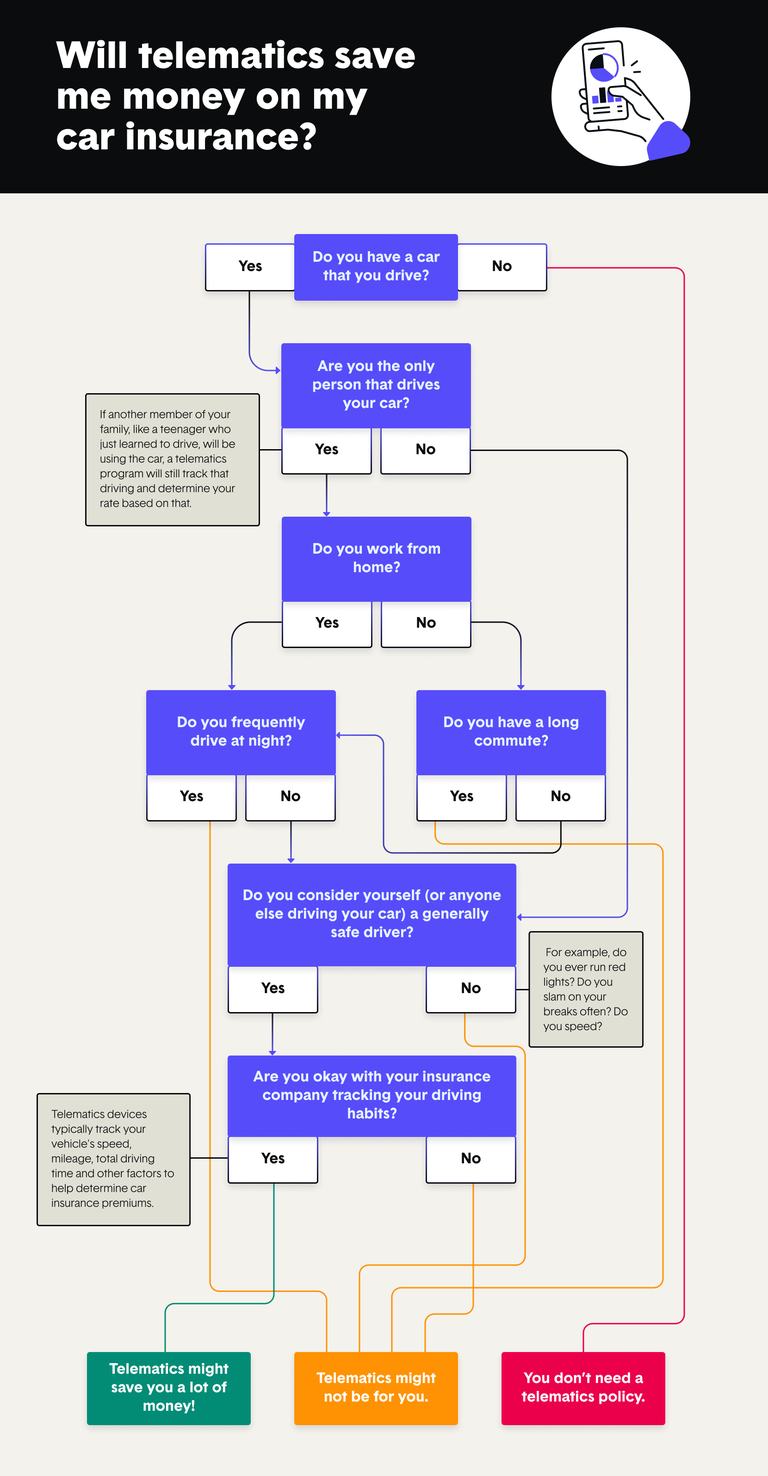

Is telematics worth it?

It depends on how you drive. Most programs are free to try, and safe driving can lead to lower rates—especially if you're typically penalized for rating factors like age or credit. Use our simple telematics decision tree below to quickly find out if a usage-based insurance plan fits your driving habits.

Telematics decision tree results explained

📝 Important note: Even if you don't fit the the "ideal" telematics profile, it could still be a good fit. Read more about the nuances of telematics below.

Ultimately, if you feel you're overpaying for car insurance, it's a good idea to see what other options are out there. We recommend checking quotes every six months. Enter your ZIP code below to see how much you could save in minutes.

Save an average of $440/year on car insurance when you compare quotes with The Zebra.

Telematics: What to know before you enroll

Telematics programs vary somewhat in how they track, score, and price your driving—so understanding the tech, trial options, and potential hiccups can help you avoid surprises.

Safe drivers can still save with telematics, even if they rack up miles. But in most programs, driving 7,000 or less often leads to bigger discounts. However, Pay-per-mile programs (like Metromile) use only mileage to set your rate — not driving behavior — and are not a good fit for high-mileage drivers.

✏️ Why it matters: You don’t need to be a weekend-only driver to benefit — but if you log serious miles, choose a program that rewards behavior, not just mileage.

Night driving (especially midnight to 5 a.m.) is considered riskier, but telematics looks at patterns, not isolated trips.

✏️ Why it matters: Occasional late drives won’t cost you — especially if the rest of your habits are strong.

Most programs use a smartphone app that works with almost any vehicle, but even those that use plug-in devices work with cars made after 1996 (with an OBD-II port). Only a few connected-car-specific programs require built-in tech (like OnStar or Blue Link). It is worth noting though that antique/classic cars may be excluded.

✏️ Why it matters: You don’t need a new or tech-heavy vehicle to take advantage of telematics.

Most track your driving and adjust your rate at renewal, though some charge monthly based on mileage (like Metromile), others set pricing after a short test drive (like Root), and some only apply discounts — never increases — at renewal (like American Family KnowYourDrive, Liberty Mutual RightTrack, and Nationwide SmartRide).

✏️ Why it matters: How your rate is set—and when it changes—can impact your budget and peace of mind. If you want predictable pricing, look for programs that only offer discounts or lock in rates after a short test drive.

That sign-up discount? It’s usually just temporary. Once your trial ends, your actual driving habits determine your rate—so safe drivers may save, but risky patterns could raise your premium.

✏️ Why it matters: Don’t assume your initial discount will last. Knowing how your program handles post-trial pricing can help you avoid surprise rate changes.

Most telematics programs let you test the waters before they impact your rate. Some offer a trial period where you can opt out with no penalty. For example, Progressive Snapshot gives you 45 days and Liberty Mutual RightTrack 90 days with no penalty.

✏️ Why it matters: There’s often low risk in trying it, especially if it’s a discount-only program.

App-based telematics is convenient, but users sometimes report battery drain, trip detection errors, or being penalized for phone use even when driving responsibly. Glitches or compatibility issues with certain phones can also affect tracking accuracy. However, in our research, all the major telematics insurance were highly rated, with most scoring between 4.5 and 4.8 stars in app stores.

✏️ Why it matters: Your rate depends on how the app interprets your driving—so tech glitches or inaccurate tracking can unfairly impact your score if you’re not paying attention.

Avoiding app pitfalls: Tips to ensure an accurate driving score

- Turn on motion detection and location services as instructed.

- Keep your phone stable (in a mount, not your hand or lap) to avoid the screen accidentally turning on.

- Ask your insurer if the app penalizes all phone use or just active interactions while driving.

- Check your trips regularly to reclassify any mistakes (like when you’re a passenger).

- Don't allow passengers to use your phone when your telematics app is in use.

- Adjust your phone settings to reduce when when the phone screen turns on.

How to find the best telematics car insurance for you

When comparing telematics programs, start by thinking about your driving habits:

- Hate being tracked all the time? Go with a program that only monitors for a short trial—like Liberty Mutual RightTrack.

- Want the biggest discount? Look for programs with higher max savings (like Nationwide SmartRide or State Farm), but check that the base price is competitive.

- Worried about your rate going up? Choose a program that only offers discounts, not penalties—like Farmers Signal, State Farm Drive Safe & Save or USAA SafePilot.

- Tend to use your phone while driving? Some programs weigh phone use heavily when calculating your score (e.g. GEICO, Progressive). While others don't track it all or track for feedback only (e.g. Nationwide, USAA), not for pricing purposes.

💡 Note: Always compare final quotes, not just discount size—a smaller discount on a cheaper base rate might still win out.

“Most telematics programs track your driving through a mobile app — and it’s important to know how to use it. If you're not the one driving (say, you're a passenger or on a train), be sure to pause tracking or reclassify the trip to avoid inaccurate scoring. Some carriers, like Progressive, make it easy to edit trips in-app.”

Riliey Culip— Licensed insurance manager at The Zebra

| Company & Program | Tracking Method | Data Collection Period | When Rate Changes | Can Increase Premiums? | Max Discount | Avg. 6-Mo Rate |

|---|---|---|---|---|---|---|

| Allstate Drivewise | Mobile app or connected car (limited makes) | Continuous | At renewal | No | -- | $996 |

| America Family KnowYourDrive | Mobile app | Continuous | At renewal | No | 20% | -- |

| Farmers Signal | Mobile app | Continuous | At renewal | No | -- | -- |

| GEICO DriveEasy | Mobile app | Continuous | At renewal | Yes | 25% | -- |

| Liberty Mutual RightTrack | Mobile app or plug-in | 90-Day Trial | After trial (locked in at renewal) | No | 30% | $608 |

| Nationwide SmartRide | Plug-in or mobile app | 4-6 mo trial | After trial | No | 40% | $696 |

| Progressive Snapshot | Mobile app or plug-in | Continuous (or 6-month trial with plug-in) | At renewal | Yes | 30% | $752 |

| Root App | Mobile app | 2-4 week "test drive" | After test drive (before policy starts) | Yes | Up to $900 per year | -- |

| State Farm Drive Safe & Save | Mobile app or connected car (OnStar, FordPass, etc.) | Continuous | Monthly and at renewal | No | 30% | $608 |

| Travelers IntelliDrive | Mobile app or (in limited states) connected car | 90-day trial | At renewal | Yes | 30% | -- |

| Travelers IntelliDrive 365 | Mobile app | Continuous | 35% | -- | ||

| USAA SafePilot | Mobile app | Continuous | At renewal | Yes | 30% | $537 |

The Zebra’s auto insurance data methodology

The Zebra’s Dynamic Insurance Rating Tool for home and auto insurance rates utilizes the latest ZIP code-level rate filings from across the U.S., sourced from Quadrant Information Services and S&P Global. These filings, typically updated annually or biennially by insurers, are verified through Quadrant’s QA process and then integrated into The Zebra’s estimator.

The displayed rates are based on a dynamic home and auto profile designed to reflect the content of the page. This profile is tailored to match specific factors such as age, location, and coverage level, which are adjusted based on the page content to show how these variables can impact premiums.

For a comprehensive understanding, see our detailed methodology.

The table above compares traditional usage-based insurance programs that monitor driving behavior. If you're more interested in plans that base your rate strictly on how much you drive, check out the following guide.

Pay-Per-Mile Car Insurance

Pay-per-mile car insurance works by tracking your mileage to determine your rate. Use our guide to learn if pay-per-mile car insurance is the best option for you.

Popular telematics programs: the details

Wondering how each program actually works? Below, we break down the key details for every major telematics provider—how they track your driving, what kind of savings to expect, and where each program is available. Expand each section to learn more about each program.

Allstate Drivewise & Milewise

Drivewise tracks your speed, braking, and time of day to reward safe driving. You'll see feedback after each trip and also benefit from their Crash Detection feature. Premiums are adjusted at renewal based on your score, and you don’t need an Allstate policy to use the app.

-

Can increase premiums: No

-

Average savings: ~$15 every 6 months

-

Average premium with Drivewise: $996

- Score is based on: Speeding (over 80 mph), hard braking, and time of day (especially late-night driving)

-

Available in: All states except CA and AK.

Milewise is Allstate’s pay-per-mile option. It’s best for low-mileage drivers and uses a plug-in device to charge a daily base rate + per-mile fee.

-

Available in: AZ, DC, DE, FL, ID, IL, IN, MD, MA, NJ, OH, OR, PA, TX, VA, WA, WV

American Family KnowYourDrive and MilesMyWay

KnowYourDrive is American Family’s behavior-based telematics program. You’ll get a 10% discount just for signing up, and safe drivers can earn even bigger savings. Your premium will never go up for participating, and discounts are applied at renewal. The program uses a smartphone app and provides feedback so you can improve your habits over time.

-

Can increase premiums: No

-

Score is based on: Hours driven, hard braking, evening and late-night driving, speeding (10+ mph over limit), phone use (screen unlocked or handheld calls), average speed, and short trips (under 5 mins)

-

Available in: AZ, CO, GA, ID, IL, IN, IA, KS, MN, MO, NE, NV, ND, OH, OR, SD, UT, WA, WI

-

Device required: No (smartphone app only)

MilesMyWay is a pay-per-mile program that rewards you for driving less—without penalizing you if you go over. Stay under 8,000 miles/year to earn up to 25% off your monthly premium. Your monthly bill is capped, so you’ll always know the most you’ll pay. It uses both a smartphone app and a Bluetooth device connected to your dash.

-

Can increase premiums: No

-

Average savings: Up to 25% (but to save 25%, you have to drive 2,000 miles or less)

-

Score is based on: Monthly mileage

-

Available in: AZ, CO, ID, IL, IN, IA, MN, MO, NE, OH, OR, SD, UT, WA, WS

-

Device required: Yes (Bluetooth device + smartphone app)

Farmers Signal & FairMile

Signal is Farmers’ telematics program for personal auto policies. It uses a smartphone app to track your mileage, time of day, speeding, and braking. Drivers get an automatic 5% discount for enrolling, and could save up to 15% at renewal based on safe driving. Young drivers under 25 may be eligible for an additional 10% discount.

-

Can increase premiums: No

-

Average savings: Up to 15%

-

Score is based on: Speeding, hard braking, mileage, and time of day

-

Available in: All states except FL, HI, NY, and SC (discount unavailable in CA)

FairMile is a separate program for small businesses with commercial auto policies. It charges based on miles driven and adjusts monthly, making it ideal for seasonal businesses or those with light driving needs. Currently only available in Washington.

Learn more about Farmers by reading our review.

GEICO DriveEasy

DriveEasy uses your smartphone to monitor driving habits and provide a real-time driving score. The app tracks behaviors like hard braking, speeding, phone use, and time of day—and even distinguishes between when you're the driver or just a passenger. GEICO is known as one of the strictest telematics programs when it comes to phone use—even quick taps or unlocking your screen while driving can lower your score. Risky driving behaviors can lead to a higher premium at renewal.

-

Can increase premiums: Yes

-

Score is based on: Phone use, hard braking, speeding, time of day, and mileage

-

Available in: All states except AK, CA, DE, HI, KS, ME, MT, NH, ND, RI, SD, and VT.

Read our in-depth guide to GEICO DriveEasy for more information.

Liberty Mutual RightTrack

RightTrack tracks your driving over a 90-day period and offers minimum 5%, maximum 30% off your premium based on how safely you drive. Most states use a mobile app, but New York regulations requires a plug-in device. Your discount is locked in at renewal and won’t be removed unless you change vehicles or policies. It's worth noting that RightTrack is typically offered only to new customers (or sometimes when making significant changes, like adding a new car).

-

Can increase premiums: No

-

Average savings: $32 to $192 every 6 months

-

Average premium with RightTrack: $448 to $608

-

Score is based on: Hard braking, rapid acceleration, nighttime driving, and mileage

-

Available in (app): AL, AR, AZ, CO, CT, DE, FL, GA, IA, ID, IL, IN, KS, KY, LA, MA, MD, ME, MI, MN, MO, MS, NE, NH, NJ, NM, NV, OH, OK, OR, PA, RI, SC, TN, TX, UT, VA, VT, WI, WV, DC

-

Available in (plug-in): NY only

See our review of Liberty Mutual.

Nationwide SmartRide & SmartMiles

SmartRide rewards safe driving with up to 40% off your premium. You get an instant 10% discount just for signing up, then Nationwide uses the app or a plug-in device to track habits like hard braking, acceleration, mileage, idle time, and nighttime driving. Idle time—like sitting in traffic—is uniquely factored in and can reduce your discount. Nationwide updates your estimated discount weekly.

-

Can increase premiums: No

-

Average savings: $18 every 6 months

-

Average premium with SmartRide: $696

-

Score is based on: Mileage, hard braking, acceleration, time of day, and idle time

-

Available in: All states except AK, HI, LA, NC, NY and OK.

SmartMiles is a pay-per-mile program designed for low-mileage drivers. Your monthly cost includes a base rate plus a variable per-mile charge, so the less you drive, the more you save.

-

Available in: All states except AK, HI, LA, NC, NY and OK.

See our review of Nationwide.

Progressive Snapshot

Progressive’s Snapshot telematics program is relatively typical among major insurers. Progressive tracks your driving with either a plug-in device or mobile app over a six-month period. Snapshot monitors when and how much you drive, along with behaviors like hard braking and rapid acceleration. Your premium can go up or down depending on how safely you drive.

-

Can increase premiums: Yes

-

Average savings: $57 every 6 months

-

Average premium with Snapshot: $752

-

Available in: All states except AK

Want more details? Read The Zebra's review of Progressive.

Or, Learn more about how Progressive Snapshot varies in your state.

State Farm Drive Safe & Save

Drive Safe & Save uses your vehicle’s OnStar system, a mobile app with a Bluetooth beacon, or connected car data (like FordPass or LincolnWay) to track your driving. The program places a strong emphasis on annual mileage, along with behaviors like braking and time of day. Your discount can reach up to 30%, and it’s updated regularly throughout the policy period based on your ongoing driving habits. For eligible Ford and Lincoln vehicles (model year 2020+), you may qualify for a connected version that transmits data automatically—no device setup needed.

-

Can increase premiums: No

-

Average savings: ~$39 every 6 months

-

Average premium with Drive Safe & Save: $608

-

Score is based on: Mileage, hard braking, acceleration, and time of day

-

Mobile app-based program available in: All states

-

Connected version available in: all states except CA, MA, RI; varies in NC

Learn more about State Farm insurance by reading our review.

Travelers IntelliDrive and IntelliDrive 365

IntelliDrive tracks your driving for 90 days using a smartphone app (or connected vehicle in some states) to calculate a discount of up to 40%. The app monitors acceleration, braking, speed, time of day, and distracted driving, including screen interaction. You can view your trips, driving score, and even track a “distraction-free streak.” You can opt out within the first 45 days, but after that, you may face a penalty if your score is low.

-

Can increase premiums: Yes (except in DC, MT, NC, and VA)

-

Score is based on: Acceleration, braking, speed, time of day, and phone distraction

-

Available in: all states except AK, AZ, CA, HI, IN, KY, LA, MI, NY, RI, UT, WV.

IntelliDrive 365 is a continuous version of the program available in AZ, IN, KY, and UT. It monitors your driving over the entire policy term, not just 90 days. You’ll get a 10% discount at enrollment and can earn up to 35% off at renewal. It uses the same scoring factors and app features as the standard version.

- Available in: AZ, IN, KY, UT

USAA SafePilot

SafePilot uses a smartphone app to monitor driving behavior and reward safe habits. You’ll get a 5% discount just for enrolling, and a larger discount is applied at renewal based on your driving score. The program tracks phone use, location, time of day, and hard braking. If there are multiple drivers on your policy, your discount is based on the average score across all drivers. While SafePilot started in just a few states, USAA has gradually expanded availability. Please note that USAA is only available to military members and their families.

-

Can increase premiums: No

-

Average savings: ~$8 every 6 months

-

Average premium with SafePilot: $537

-

Score is based on: Phone use, hard braking, location, and time of day

-

Available in: all states except CA, DE, and NJ

Read our full USAA review for more information on USAA's insurance offerings.

SafePilot Miles is USAA’s pay-per-mile insurance program designed for low-mileage drivers. Your premium includes a base rate plus a variable rate that changes based on how much you drive each month. Drivers can save up to 20% for driving fewer miles, and an additional up to 20% earned discount is available for safe driving behavior. All drivers must use the mobile app to track mileage and habits and the discount will be determined by the average behaviors of all listed drivers.

Compare rates today and see if you can save more with telematics or a traditional policy!

Typical telematics auto insurance discounts by state

Telematics programs can work differently depending on where you live. Here are a few state-specific quirks to keep in mind:

-

California: Prohibits telematics-based pricing—programs are extremely limited.[3]

-

North Carolina and New York: Telematics can’t raise your premium—only discounts are allowed.[4]

-

Maryland: Considering legislation to limit telematics use to discounts only (would be enacted in October 2025).[5]

Now that you know how rules can vary, here’s a look at the average annual savings drivers receive from telematics-based car insurance in each state.

Source: The Zebra

Frequently asked questions about useage-based car insurance

-

Insurance Telematics Market. Fortune Business Insights.

Insurance Telematics Market. Fortune Business Insights.

-

Data Methodology. The Zebra’s Dynamic Insurance Rating Tool

Data Methodology. The Zebra’s Dynamic Insurance Rating Tool

-

Proposition 103. California Department of Insurance

Proposition 103. California Department of Insurance

-

NC Answers: Why are some safe driving insurance discounts not allowed in North Carolina?Citizen Times

NC Answers: Why are some safe driving insurance discounts not allowed in North Carolina?Citizen Times

-

SB0984. Maryland General Assembly

SB0984. Maryland General Assembly

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.