The United States looked different in the 1960s, a time of visionaries, idealists, and growing prosperity. Rapid changes in technology have re-shaped much of American life, including how we socialize, work, and travel.

Many significant changes in the lives of Americans since 1960 involve the home: Where we live, how we live and who we live with are all very different now than they were 60 years ago.

For example, while rural areas of the United States have maintained roughly the same population (54 million in 1960 and 57 million in 2020), urban areas have gained nearly 150 million inhabitants in the last six decades.

As experts in the world of home insurance, we wanted to dig deeper into the ways that housing has affected the lives of Americans both historically and in the present. Using U.S. Census Bureau data, we explored how housing has changed for Americans since 1960.

Some of our key findings include:

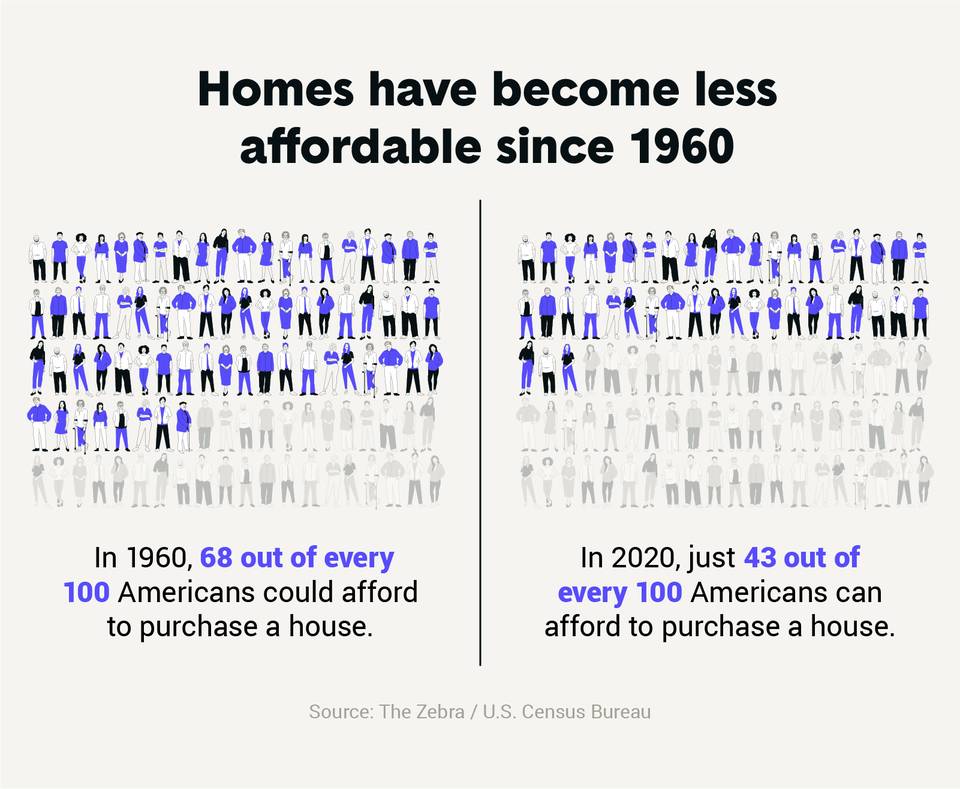

- Homes have become less affordable: In 1960, approximately 68 out of 100 Americans could afford a home, but now only around 43 out of 100 can afford one.

- Homeownership disparity has increased slightly: In the last 60 years, the homeownership gap between white and Black Americans has widened slightly from 26% to 29.4%.

- Single-person households are more common: The number of Americans living alone has increased dramatically, from 6.4% to 23%.