Cheap Car Insurance for 23-Year-Olds

- 23-year-old drivers on average pay $977 per 6-month policy.

- GEICO and Nationwide offer the cheapest auto insurance for 23-year-olds, but factors like driving record, location, and coverage level will influence your rate.

![]() Why you can trust The Zebra

Why you can trust The Zebra

Ava joined The Zebra in 2016 as a licensed insurance agent and writer. She now serves as director of insurance content, leading coverage strategy and…

- 9+ years of Experience in the Insurance Industry

What's the average car insurance rate for 23-year-olds?

The average 23-year-old driver pays $977 in insurance premium for a six-month car insurance policy in the US. Compared to the overall average auto insurance rate, this is $235 more expensive. Finding affordable auto insurance as a young driver under 25 years old can be difficult — especially if you’re a young male driver.

In the eyes of auto insurance companies, a younger driver in their 20s still carries a decent amount of risk even if they've aged out of being a teenage driver. Insurers will therefore charge a higher car insurance premium for younger drivers to account for the possibility of them getting into accidents or receiving tickets and citations.

Let’s explore some cheap car insurance companies for 23-year-olds — as well as auto insurance rates from popular companies — and some additional ways to save and discounts.

Cheapest companies by gender

Males

We discovered GEICO and USAA are the cheapest companies for a 23-year-old male. USAA will set you back $1,822 in car insurance cost for an annual or $152 per month. If you do not qualify for USAA (you must be a military member or family of one to qualify) GEICO costs an average of $1,970 per year — just $12 more than USAA per month.

This data is reflective of a very generalized profile throughout the US and should only be considered directionally. You should also consider each car insurer's customer satisfaction rating.

Updating data...

| Company | Avg. Annual Premium | Avg. Monthly Premium |

|---|---|---|

| USAA | $1,822 | $152 |

| GEICO | $1,970 | $164 |

| Nationwide | $2,104 | $175 |

| State Farm | $2,332 | $194 |

| Farmers | $2,443 | $204 |

| Progressive | $2,575 | $215 |

| Allstate | $3,411 | $284 |

Source: The Zebra

Females

If you’re a 23-year-old female, the average cost for insurance will actually be slightly cheaper than the rates we displayed above. Because of their risk profile, young female drivers are charged less for car insurance than men.

On average, a 23-year-old woman will pay $2,280 per year. Consider starting your search for auto insurance with GEICO or USAA — these companies again proved to be the most affordable options for 23-year-old female drivers.

Updating data...

| Company | Avg. Annual Premium | Avg. Monthly Premium |

|---|---|---|

| USAA | $1,722 | $144 |

| GEICO | $1,858 | $155 |

| Nationwide | $1,957 | $163 |

| State Farm | $2,064 | $172 |

| Farmers | $2,294 | $191 |

| Progressive | $2,404 | $200 |

| Allstate | $3,014 | $251 |

Source: The Zebra

The Zebra’s Dynamic Insurance Rating Tool data methodology

The Zebra’s Dynamic Insurance Rating Tool for home and auto insurance rates utilizes the latest ZIP code-level rate filings from across the U.S., sourced from Quadrant Information Services and S&P Global. These filings, typically updated annually or biennially by insurers, are verified through Quadrant’s QA process and then integrated into The Zebra’s estimator.

The displayed rates are based on a dynamic home and auto profile designed to reflect the content of the page. This profile is tailored to match specific factors such as age, location, and coverage level, which are adjusted based on the page content to show how these variables can impact premiums.

For a comprehensive understanding, see our detailed methodology.

Get auto insurance for 23-year-olds today!

How 23-year-olds can save on car insurance

The best way to save is to follow our suggestion above and shop around as much as possible, in addition to maintaining a clean driving record. Discounts and changing your coverage can only save you so much in premium. More often than not, you’re paying too much money on car insurance because your company is overpriced. Still, there are some tips we should outline.

Avoid claims

Most insurance companies will charge you for three to five years after you’ve filed a claim. Depending on the value of the damage, the surcharge could be greater than simply paying for the damage yourself. If you’ve damaged your own vehicle, follow our steps before contacting your insurance company.

- Get a cost estimate for the damage independently.

- Use The Zebra's State of Insurance analysis to see how much an at-fault accident would raise rates in your state. Again, consider this surcharge for over three years.

- Compare the three-year surcharge value plus your deductible to the out-of-pocket expenses you learned in step one. If it is cheaper to pay for your claim out-of-pocket, do just that instead of going through insurance and facing a rate increase.

For example, you get into a car accident and cause $1,000 worth of property damage to your vehicle. You have a collision deductible of $500 and the average rate increase for an at-fault accident where the damage amounts to between $1,000-$2,000 is $630 annually. Factoring in a three-year accident surcharge and your deductible, you would end up paying $2,390 for a claim that would have only cost $1,000 to repair out-of-pocket. In this sense, it would cost you more overall to file a claim.

See more information on whether or not to file a claim.

Adjust your coverage

If your vehicle is worth less than $4,000, consider if you still need comprehensive and collision coverage. These coverages are designed to protect the physical integrity of your vehicle. However, if your vehicle isn’t particularly valuable, you could be paying for insurance coverage you do not need. It may be sufficient to only carry liability coverage. Get an estimate for your vehicle by using Kelley Blue Book and NADA online.

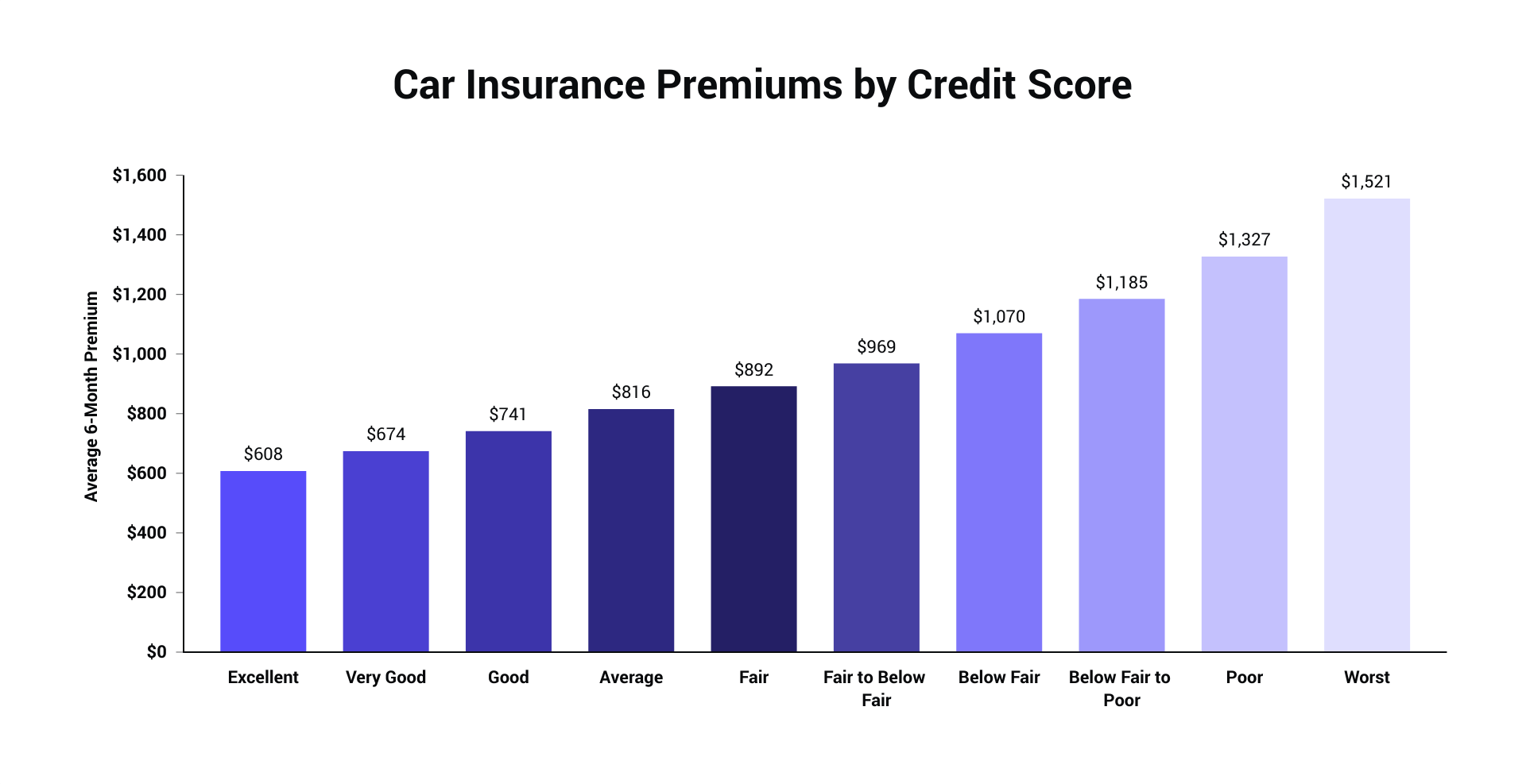

Be mindful of your credit score

Whether you know it or not, your credit score has a major impact on what you pay for car insurance. Insurance companies see a correlation between a poor credit score and proclivity for filing costly claims. As such, they charge higher premiums for clients with poor credit. On average, if you can improve your credit score from Poor to Excellent you can decrease your premium by more than double what you were paying. Just another reason to keep your credit score high!

Finding cheap car insurance with bad credit is difficult, but not always a death sentence. See more info on how to find auto insurance with bad credit.

Keep your grades up

If you’re still in college and have above a 3.0 GPA, you should look into getting what’s called a Good Student Discount. Insurance companies see students with above B averages as less risky drivers and thus better clients. Often grouped together with a Defensive Driver Discount, you can expect an average savings of $119.

| Age | Male | Female |

|---|---|---|

| 22 | $176 | $103 |

| 23 | $151 | $88 |

| 24 | $135 | $78 |

Stay in touch and subscribe!

Get advice, insights and tips from our newsletter.

Avoid high-value vehicles

It’s important to consider the relationship you and your vehicle have in terms of auto insurance. Pairing a risky driver with a high-value vehicle is always going to be more expensive than if the same driver drove a more moderate vehicle. While you don't need to opt for the cheapest car possible, driving something like a modest lightly-used sedan will help you cut down the cost of car insurance.

Look for discounts

There are a few discounts that can help 23-year-old drivers save money. Let’s break them down:

- Defensive driver discount - This discount is offered to those taking a professional driving course. It's aimed at making you a smarter and better driver. Again, you would need to prove you have completed the course prior to receiving the discount.

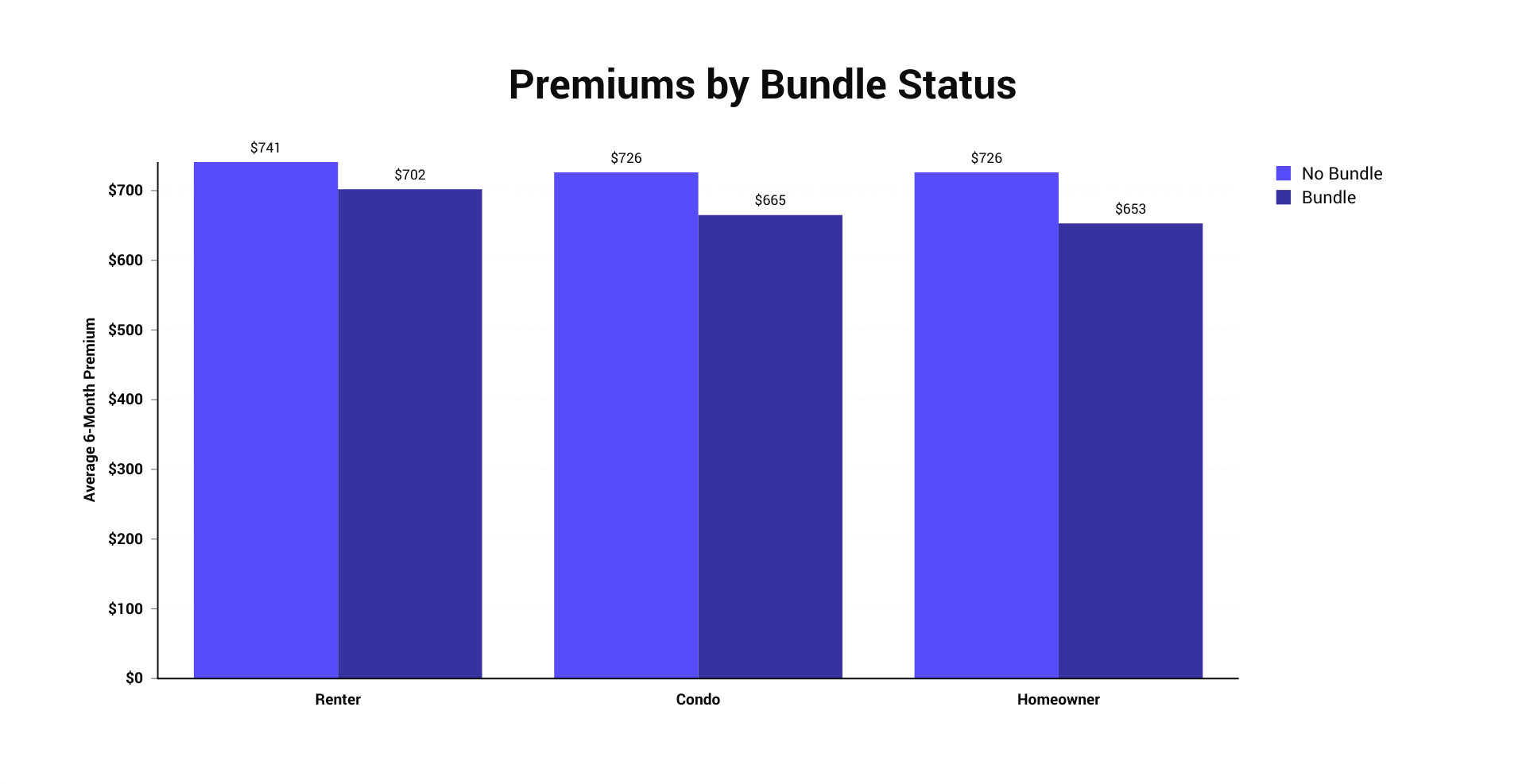

- Bundling your policies - If you rent a house or apartment, you should bundle your renter’s policy and your auto policy with the same company in order to earn a multi-policy discount. This is a great way to reduce the number of insurance companies you have to deal with and save a few bucks.

Consider telematics

Telematics, or usage-based insurance, are in-vehicle devices that use the way you drive to determine your premium. In theory, if you’re a safe driver (no harsh braking, rapid acceleration, etc.), you can earn a discount on your premium. Below are some advertised discounts by popular insurers.

| Program | Average Savings |

|---|---|

| Progressive SnapShot | Average of $130 |

| GEICO DriveEasy | Varies |

| Allstate DriveWise | Average of 10-25% |

| State Farm Drive Safe & Save | Up to 15% |

| Esurance DriveSense | Varies |

| Nationwide SmartRide | Up to 40% |

| Liberty Mutual RightTrack | Average of 5-30% |

| Root Car Insurance | Varies |

| Metromile | Varies |

Car insurance for 23-year-olds: to summarize

At the end of the day, your best bet for finding affordable rates at this age is to compare car insurance quotes with as many companies as possible. Getting quotes will not impact your credit score nor will it affect your current rate. If you’re interested in seeing rates from local and national auto insurance companies, enter your ZIP code below to get started.

Compare rates quickly and easily!

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.