Car Insurance in Queens, NY

![]() Why you can trust The Zebra

Why you can trust The Zebra

Kristine joined The Zebra in 2019 as an in-house content researcher and writer, with a property and casualty insurance license. Before joining The Ze…

- Licensed Insurance Agent — Property and Casualty

- 6+ years of Experience in the Insurance Industry

Ross joined The Zebra as a writer and researcher in 2019. He specialized in writing insurance content to help shoppers make informed decisions.

Ross h…

- 5+ years in the Insurance Industry

Queens car insurance

Car insurance is very expensive in New York City's second-most populous borough — Queens insurance premiums are almost double the average rate in the state of New York and 115% more expensive than the national average.

Insuring a car in Queens is typically 62% cheaper than in Brooklyn, which holds the title for NYC's most expensive auto insurance rates. However, the average premium in Queens still runs a pricey $278 per month, so it's of the utmost importance to save where you can. Consult our guide to Queens auto insurance so you know what a fair rate looks like for your budget.

| Location | 6-Month Premium |

| US | $774 |

| New York | $852 |

| Queens | $1,665 |

Average rates by car insurance company

Looking at how expensive it is to insure a vehicle in Queens — and in NYC, in general — you may be wondering: why? What makes insurance costs rise in certain locations?

This has to do with the way insurance companies gauge risks to predict potential future losses in the area. Taking into account factors like population size and density, crime rates, weather-related hazards, and claims histories down to specific ZIP codes, insurers generally view Queens as a riskier place to drive and own a car. They make up for this elevated risk by charging higher premiums for drivers.

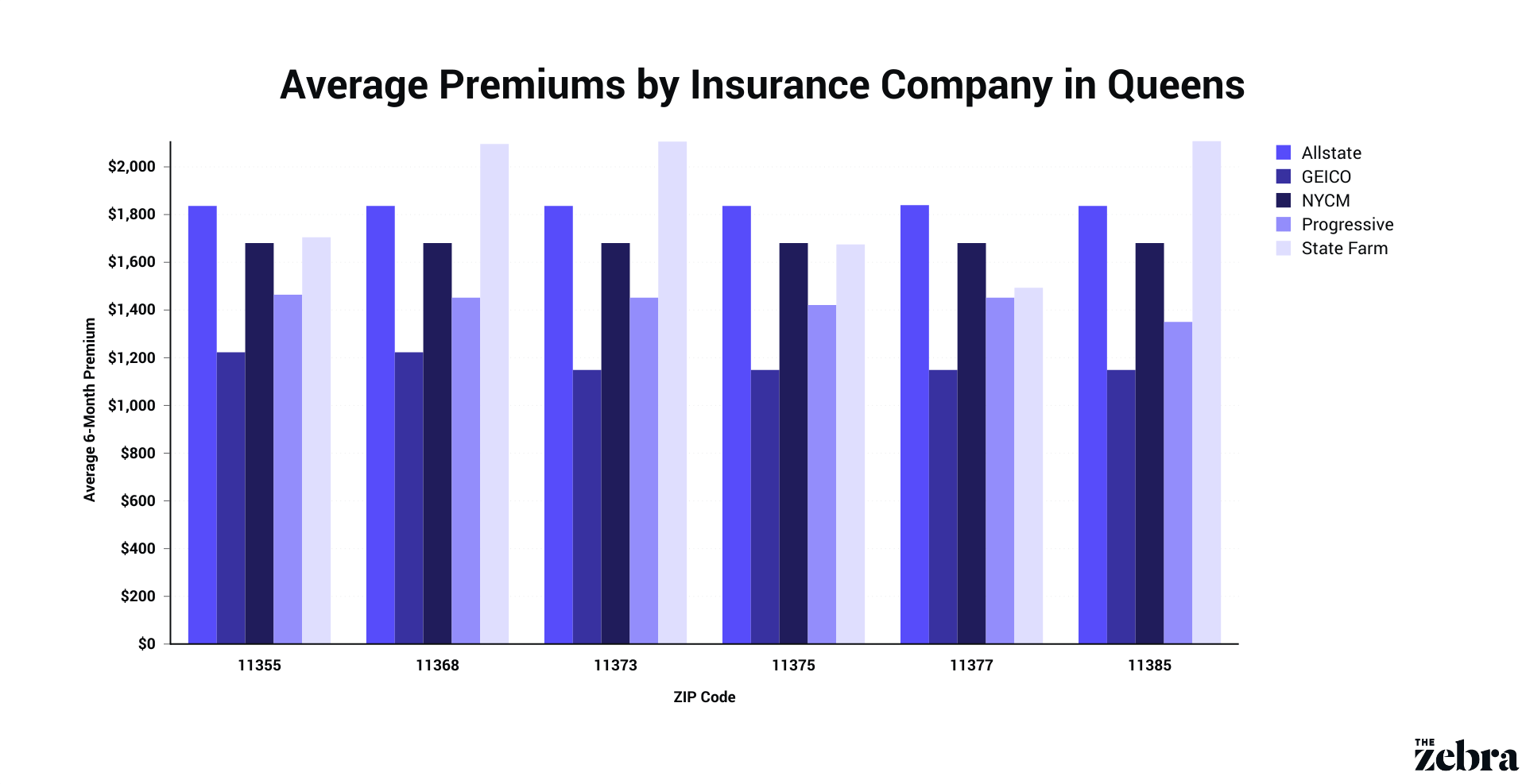

We surveyed six ZIP codes in the borough of Queens to map out average car insurance rates by company. Here are the results:

Using the sample driver profile from our methodology, we found GEICO was the cheapest insurance company. At a monthly cost of $195, GEICO was 43% cheaper than the Queens average. Progressive was the second-cheapest. See the table below to see average six-month premiums across the Queens area.

| Insurance Company | Average 6-Month Premium |

| Allstate | $1,797 |

| GEICO | $1,316 |

| New York Central Mutual (NYCM) | $1,810 |

| Progressive | $1,468 |

| State Farm | $1,933 |

Use this data as a starting point in your search for cheap car insurance in Queens, keeping in mind that your rate may vary since your driver profile likely does not match ours exactly (30-year-old male driving a Honda Accord). Enter your ZIP code below to compare auto insurance quotes and find the best deal on your next policy.

Compare quotes to find the cheapest car insurance in Queens!

How to save on auto insurance

It's no secret NYC is an expensive place to live, let alone own a car. If you plan on driving in Queens, take note of these expert tips on how to save money on car insurance.

Double-check for discounts

Many discounts provided by insurance companies are automatically built into your rate. However, the number of discounts tends to vary from company to company, so make sure you do your research and ask about any cost-cutting measures that will bring down your premium. Common car insurance discounts include:

- Bundling

- Good student

- Good driver

- Paid in full, electronic funds transfer (EFT), electronic signature

- Safety equipment

Individually, these discounts aren't very steep but they do add up to help make your premium more affordable over the long run.

Drive safely

One of the most important factors in keeping your premium as low as possible is your driving record. The financial consequences of infractions and violations like at-fault accidents, DUIs, and reckless driving can be severe, and citations will stay on your record for three years in most states. You can save thousands of dollars over the surchargeable three-year period if you maintain a good driving history.

AVERAGE ANNUAL INCREASE BY VIOLATION

| Violation | Increase to Premium |

| At-Fault Accident | +$912 |

| Hit and Run | +$1,868 |

| Racing | +$1,373 |

| Reckless Driving | +$1,373 |

| Speeding Ticket | +$479 |

| DUI/DWI | +$1,656 |

Maintain a good credit score

The difference between what a driver with bad credit pays versus someone with excellent credit is over a whopping $4,500 per year in Queens. It is critical to keep a decent credit score if you're looking to lower your premium. Even improving your credit from Fair (580-669) to Very Good (740-799) can yield a savings of over $1,800 annually.

Take advantage of bundling

If you need more than one insurance policy — say, homeowners insurance plus auto — definitely look into acquiring both through a single insurance company to get a bundling discount. This is one of the most common discounts and is typically offered at any reputable insurance company.

Renters in Queens can save $150 every year by bundling renters insurance with car insurance.

Be smart with your auto insurance coverage

With each passing year, the worth of your vehicle will depreciate. This means that the full coverage you once had on your brand new leased or financed car will no longer be necessary once that car reaches about 10 years of age and/or is worth less than $4,000. The physical protection provided by comprehensive and collision coverages isn't legally required like liability insurance is. Liability coverage protects other drivers from property damage and bodily injury that you cause in an at-fault car accident.

At a certain point in the lifespan of your car, it's simply not worth paying for these coverages if your vehicle isn't worth much. In addition, you can save over double your premium by dropping these coverages in favor of liability-only.

We recommend using resources like Kelley Blue Book and NADA online to find out what your vehicle is worth. If you decide to drop comprehensive and collision, consider adding uninsured motorist coverage instead. This will protect you from uninsured or underinsured drivers and hit and runs.

Be smart with your claims

Knowing what's worth filing a claim for and what's not is integral to keep your premiums low, but also to keep your options open when it comes to switching insurers. A lengthy claims history is a red flag to many insurance companies, and some may not be willing to offer coverage if you have one too many claims on your record.

Most violations, tickets and claims will stay on your record for three years. This also means that you will be charged an increased rate over that period. You will need to consider if the amount you would save by filing a claim is worth the cumulative sum of your premium increase. In Queens, the average yearly increase for an at-fault accident was $912. Compounded over the three-year chargeable period, that's a total of over $2,700 in excess premium.

Unsure of when to file a claim? We suggest starting with these tips:

- Get an estimate at a local repair shop in Queens.

- Consider if the value of the damage is over $2,736 in addition to your deductible — if it's less than the total out-of-pocket expense, it makes sense to file that claim.

Compare rates

In the end, some insurance companies tend to be more expensive than others, try as you might to improve all of the relevant rating factors used in calculating premiums. The best way to nail a good deal on car insurance — no matter what kind of driver you are — is to shop with as many companies as possible.

The Zebra makes it easy to compare customized insurance quotes from companies across the nation, and takes most of the legwork out of the shopping process. Enter your ZIP code below to start comparing car insurance quotes side-by-side.

Find an auto insurance policy today!

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.