How to Read a Homeowners Insurance Policy

A homeowners insurance policy outlines your dwelling, personal property, liability, and additional living expense coverage, along with exclusions, conditions, and endorsements.

Knowing how to understand it will help you be prepared in the event of a home claim.

![]() Why you can trust The Zebra

Why you can trust The Zebra

Ross joined The Zebra as a writer and researcher in 2019. He specialized in writing insurance content to help shoppers make informed decisions.

Ross h…

- 5+ years in the Insurance Industry

Beth joined The Zebra in 2022 as an Associate Content Strategist. A licensed insurance agent, she specializes in creating clear, accessible content t…

- Licensed Insurance Agent — Property and Casualty

- Associate in Insurance (AINS)

- Professional Risk Consultant (PRC)

- Associate in Insurance Services (AIS)

Renata joined The Zebra in 2020 as a Customer Experience Agent. Since 2021, she has worked as a licensed insurance professional and content strategis…

- Licensed Insurance Agent — Property and Casualty

- 5 years of experience in the insurance industry

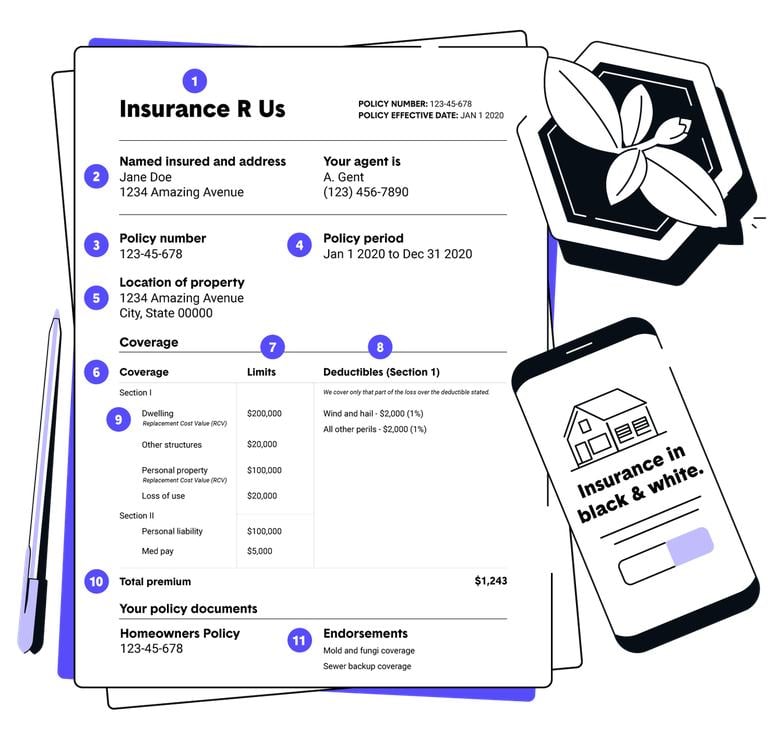

How to read a homeowners insurance declaration page

Your home is one of the biggest investments you’ll ever make, and the right insurance helps protect it. But homeowners insurance documents can be confusing, especially since every insurer formats them differently. This guide breaks down what’s on your declaration page and shows you how to make sure your home and belongings are properly covered.

What is a homeowners insurance declaration page?

Each section of your homeowners policy is important, but the declaration page (often called a dec page)is likely your go-to source for most information. Here you’ll find important info about your coverage amounts, coverage limits, and insurance premiums.

Take a look at the example below to learn more about standard features of a homeowners declaration page.

- Insurance company: The name of your insurance provider.

- Named insured: Holder of the policy.

- Policy number: This unique policy number is needed anytime you file a claim.

- Policy period: Lists the start and end dates of your policy.

- Policyholder address: Location of the insured property.

- Coverages: This section details the specific coverages included in your policy.

- Limits: Signifies the limits of each coverage.

- Deductibles: The amount for which you're responsible for paying before your insurance coverage kicks in. A higher deductible can lead to lower monthly insurance rates.

- Replacement cost value/actual cash value: This signifies whether the insurance company will factor in depreciation when covering your losses or replace them at the full value.

- Total premium: The total amount due over the duration of the policy term.

- Endorsements: Additional coverages and customizations.

Ready to find better home coverage?

Homeowners insurance coverage types explained

There can be many different coverage types within a single homeowners policy. The following list provides a brief rundown of each and how they work to protect you and your property.

Coverage A: Dwelling

Dwelling coverage pertains to the primary dwelling and attached structures such as fences or garages.

Coverage B: Other structures

This includes detached structures such as sheds or detached garages. The limit of this coverage is 10% of your Coverage A limit.

Coverage C: Personal property

This covers your home’s contents or other personal property. This also covers personal belongings you carry while traveling. The limit of this coverage is 50% of your Coverage A limit. Another important thing to consider is the amount at which your belongings will be replaced. Actual cash value is standard amongst many policies, though full replacement cost coverage can typically be added at an additional cost.

Coverage D: Loss of use

Loss of use provides coverage in the event your home is rendered unfit to live in. It covers additional living expenses and will pay for temporary living arrangements up to the policy limit.

Coverage E: Personal liability

Liability coverage is a vital component of a homeowners insurance policy. It protects you against damages or injuries caused by you or occurring on your property. Liability insurance follows you around the world as well, meaning you would be covered— in most cases — if you were to accidentally injure someone else while on vacation. In some cases, an umbrella policy can be added to provide increased personal liability protection.

Coverage F: Medical payments to others

This coverage covers some of the medical expenses of others who may have suffered bodily injury or property damage at your home. Sometimes known as guest medical coverage, it usually provides a baseline of $1,000 in coverage that can often be increased for an additional premium.

How to Read a Car Insurance Policy

Make sure you know where to find important information on your policy documents.

Actual cash value/replacement cost value

Many basic policies cover a home and the personal property therein at actual cash value. Actual cash value factors in depreciation when considering how much to pay out for a covered loss. On the other hand, replacement cost value covers the actual cost to replace your dwelling or personal property without factoring in depreciation. This can be added for an additional premium.

"With actual cash value (ACV), depreciation kicks in fast, and you could end up paying most of the repair bill out of pocket. That applies to personal belongings too. You want to make sure your policy is written with replacement cost (RCV) coverage across the board, including for the home itself."

-Johnny Hawkins, Manager and Licensed Agent at The Zebra

Home insurance endorsements

Endorsements to a home insurance policy allow you to customize your coverage to fit your individual needs. These add-ons can provide additional coverage to allow for unique needs in your lifestyle or geographic location. Common endorsements can include coverage for windstorms, identity theft, and home daycare coverage, to name a few.

You can also add personal property endorsements (also known as scheduled endorsements) to increase coverage limits for high-value items such as antiques or jewelry. This often requires an appraisal of the items and an agreement from the insurance company on the payout amount.

One marketplace for top providers

Homeowners insurance required by mortgage lenders

Also listed on your insurance policy will be the name of your mortgage lender. Mortgage lenders often have their own insurance requirements to protect their investment in the event of a loss. The types of coverage required may vary depending on your lender and are likely to be based on the type of home you have as well as its location.

What perils does your homeowners policy cover?

Sometimes, dwelling and personal property coverage differ in the perils they cover. For instance, an HO-3 policy (the most common home insurance policy type) covers personal belongings on a named peril basis.

Common perils named on most HO-3 policies include:

- Lightning or fire

- Hail or windstorm

- Damage caused by aircraft

- Explosions

- Riots or civil disturbances

- Smoke damage

- Damage caused by vehicles

- Theft

- Vandalism

- Falling objects

- Volcanic eruption

- Damage from the weight of snow, ice, or sleet

- Water damage from plumbing, heating, or air conditioning overflow

- Water heater cracking, tearing, and burning

- Damage from electrical current

- Pipe freezing

Pay close attention to which perils your policy covers: this can have consequences down the line.

Home insurance policy exclusions

Every home insurance policy has exclusions. While an HO-3 policy covers your personal belongings against named perils, it covers your primary dwelling on an open peril basis. This means that it will cover damage caused by all perils except those explicitly listed in this section of the policy.

An HO-3 policy specifically excludes damages caused by the following perils:

- Freezing pipes and systems in vacant dwellings

- Damage to foundations or pavements from ice and water weight

- Theft from a dwelling under construction

- Vandalism to vacant dwellings

- Latent defects, corrosion, industrial smoke, pollution

- Settling, wear, and tear

- Pets, other animals, and pests

- Weather conditions that aggravate other excluded causes of loss

- Government and association actions

- Defective construction, design, and maintenance

Flood insurance: This covers damage resulting from flooding. Flood coverage is generally an excluded peril, as most standard homeowners policies do not include it. While it is offered by some specialty insurers, it is most often purchased through the National Flood Insurance Program (NFIP).

Home insurance discounts

Many homeowners insurance companies offer discounts that can save you money on your insurance premiums. Installing deadbolt locks or a security system to deter burglars can lead to lower insurance rates. Bundling your home insurance with your auto insurance can likewise lead to savings. Below is a list of common discounts offered by most home insurers. Speak to your insurance company or agent to see which discounts you are eligible for.

- Loyalty discount

- Multi-policy discount

- Home security system discount

- Fire prevention discount

- Retired or mature discount

- Occupation-based discounts

- Discounts for going claims-free

Homeowners policy considerations

Understanding your policy is key to protecting your home. Your declaration page gives an overview of coverage, but it’s important to read the full policy to spot any gaps. When shopping, compare rates and coverage details to find the best fit before choosing a provider.

When it comes to insurance, we have you covered

Reading homeowners insurance policies FAQs:

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.