Home Insurance for Older Homes

Older homes come with some special considerations when it comes to homeowners insurance.

![]() Why you can trust The Zebra

Why you can trust The Zebra

Kristine joined The Zebra in 2019 as an in-house content researcher and writer, with a property and casualty insurance license. Before joining The Ze…

- Licensed Insurance Agent — Property and Casualty

- 6+ years of Experience in the Insurance Industry

Renata joined The Zebra in 2020 as a Customer Experience Agent. Since 2021, she has worked as a licensed insurance professional and content strategis…

- Licensed Insurance Agent — Property and Casualty

- 5 years of experience in the insurance industry

Homeowners insurance for older houses

Beneath the charming facade, appealing architectural features and historic significance of many older homes lies a certain amount of risk that causes insurance companies to hesitate before offering coverage to homeowners. Due to the varying degrees of care or neglect seen in the long-term maintenance of an old house, these homes may be cheaper to buy but more expensive to insure than a new build.

Another contributing factor is the added expense of repairing an older home, as essential components like plumbing, wiring and building materials may not be modern. Some insurance companies may even refuse to insure homes with pre-existing damage to the roof or the dwelling’s structure.

In our guide to finding homeowners insurance for older homes, we’ll cover average costs, coverage options to consider and the best ways to save money on your premium.

Key takeaways

- Older homes are typically cheaper to buy but more expensive to insure.

- An HO-8 policy is specifically tailored to older homes with materials that are difficult to replace.

- The cheapest home insurance company for older homes is Amica.

How much does home insurance cost for older houses?

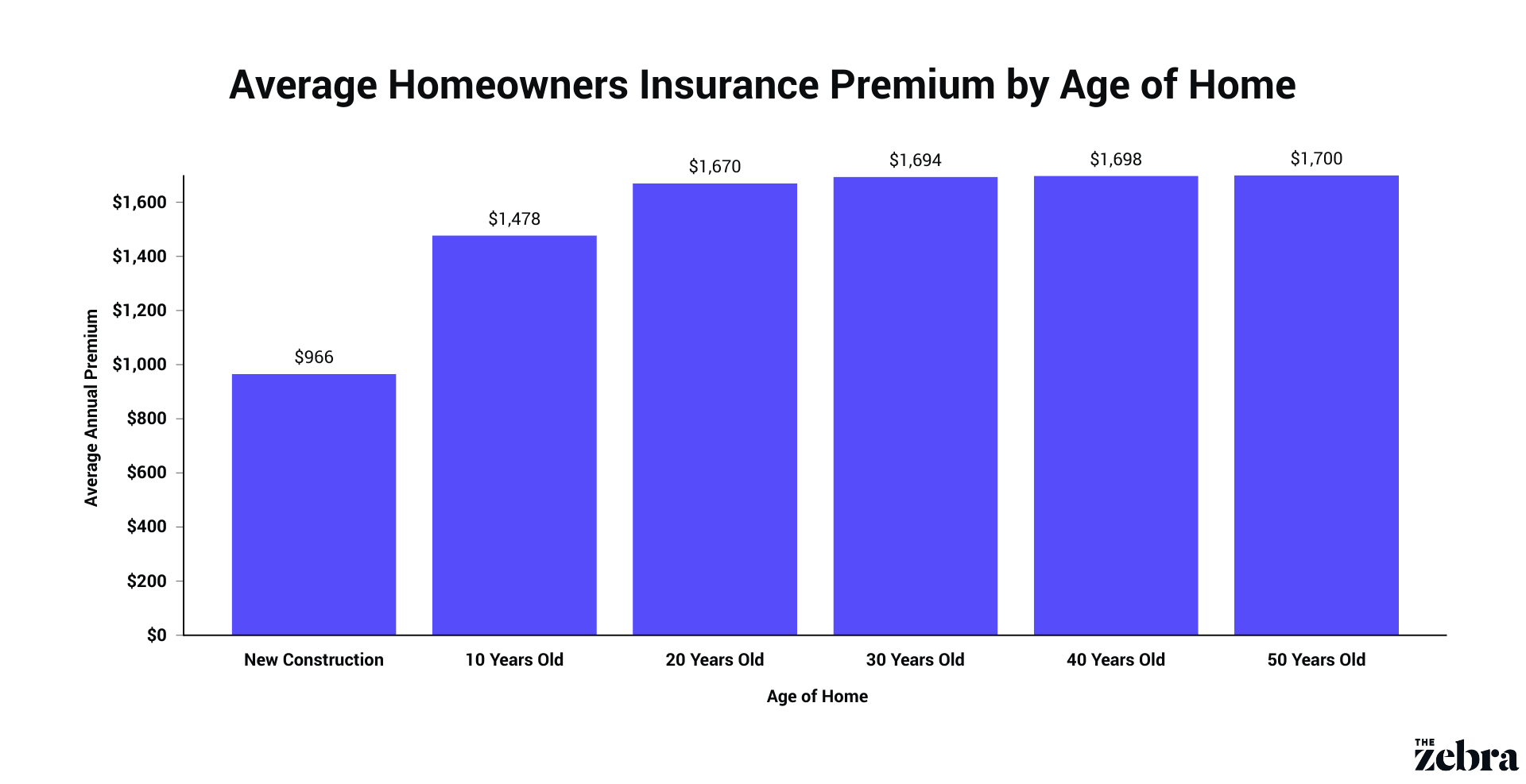

The average insurance premium for a home older than 30 years is 75% more expensive than the average rate for a newly constructed home. The most substantial increase in home insurance rates occurs once your home reaches 10 years of age. Rates creep up incrementally as your home ages.

Expect to pay at least $1,600 a year for homeowners insurance and use this data as a jumping-off point in your search; because myriad factors go into home insurance rates, the profile used in our methodology may not align with yours.

| Age of Home | Average Annual Premium | Monthly Premium | % Difference |

|---|---|---|---|

| New construction | $966 | $80 | - |

| 10 years old | $1,478 | $123 | +53% |

| 20 years old | $1,670 | $139 | +13% |

| 30 years old | $1,694 | $141 | +1% |

| 40 years old | $1,698 | $142 | +0.23% |

| 50 years old | $1,700 | $142 | +0.12% |

The Zebra’s homeowners insurance data methodology

The Zebra’s Dynamic Insurance Rating Tool for home and auto insurance rates utilizes the latest ZIP code-level rate filings from across the U.S., sourced from Quadrant Information Services and S&P Global. These filings, typically updated annually or biennially by insurers, are verified through Quadrant’s QA process and then integrated into The Zebra’s estimator.

The displayed rates are based on a dynamic home and auto profile designed to reflect the content of the page. This profile is tailored to match specific factors such as age, location, and coverage level, which are adjusted based on the page content to show how these variables can impact premiums.

For a comprehensive understanding, see our detailed methodology.

Insurance companies for older homes

While rates might be higher for older homes, it is still possible to find homeowners insurance with many major and regional companies. Let's take a look at some of the nationwide insurance companies and their rates by home age.

What are the cheapest home insurance companies by home age?

- New construction — Progressive

- 10 to 50 years old — Amica

| Insurance Company | New Construction | 10 Years Old | 20 Years Old | 30 Years Old | 40 Years Old | 50 Years Old |

|---|---|---|---|---|---|---|

| Allstate | $1,033 | $1,594 | $1,709 | $1,755 | $1,750 | $1,759 |

| American Family | $1,422 | $2,261 | $2,396 | $2,405 | $2,409 | $2,422 |

| Amica | $772 | $1,089 | $1,145 | $1,152 | $1,152 | $1,144 |

| Farmers | $1,093 | $1,455 | $1,606 | $1,553 | $1,539 | $1,516 |

| Nationwide | $693 | $1,236 | $1,447 | $1,487 | $1,524 | $1,542 |

| Progressive | $533 | $1,355 | $1,913 | $1,941 | $1,884 | $1,810 |

| State Farm | $885 | $1,356 | $1,520 | $1,524 | $1,531 | $1,532 |

| Travelers | $929 | $1,444 | $1,671 | $1,716 | $1,703 | $1,692 |

| USAA | $706 | $1,231 | $1,477 | $1,484 | $1,495 | $1,475 |

Why are older homes more expensive to insure?

The replacement cost of an older home is more expensive than that of a newer home — even if they have similar market values. This is because old homes incorporate more customizations and special features than new structures, and can be built from antiquated or obsolete building materials (like plaster walls) that are pricier to repair or replace if damaged.

For instance, if you’re considering purchasing a historic Victorian home, you’ll need to consider that the cost of replacing electrical systems, plumbing systems, walls and roofing with more modern materials that meet building codes could get expensive. On top of that financial burden, you may have trouble finding homeowners insurance if the home isn’t maintained to your insurer’s standards.

What homeowners insurance policy covers older homes?

An HO-8 insurance policy specifically covers older homes that are difficult to replace — generally, these are properties where the home’s replacement value exceeds its market value. This is a modified form of an HO-3 homeowners policy for those who own houses that are more than 40 years old. This insurance coverage protects the structure of your dwelling in addition to your personal liability and personal property.

However, HO-8 policies don’t operate on replacement cost — if a special architectural feature of your home is damaged, your insurance company will pay out based on actual cash value, deducting for depreciation in your claim payout and leaving you on the hook to cover the remaining amount of damage.

To guarantee that your historic home is rebuilt fully should disaster strike, you may need to look into high-value homeowners insurance. Insurance companies well-versed in covering high-value properties may also be more familiar with older, historic homes. It's important to understand the details of your homeowners policy to make sure you're not underinsured— the Insurance Information Institute[1] offers a handy checklist and is a good place to start

Curious to see what you could be paying for homeowners insurance? No matter the age of your home, it never hurts to look and shop around. Enter your ZIP code below to compare insurance quotes, or continue reading to explore coverage considerations and how to save money on insuring your older home.

Compare home insurance quotes quickly and easily.

Home insurance coverages to consider for old or historic homes

The standard coverages included in a home insurance policy may not be sufficient to fully protect an older home — especially if it’s historic or high-value. Below are some coverage options that can typically be added as an endorsement, allowing you to fortify your home insurance policy with some additional coverage.

Replacement cost coverage

As previously mentioned, though HO-8 policies cater to older homes, a significant shortcoming of this policy type is that it pays out based on actual cash value which deducts for depreciation. Opting for replacement cost coverage instead is a great start in protecting your home, but a homeowner can take it a step further by acquiring guaranteed or extended replacement cost coverage. Guaranteed replacement cost extends your coverage limits to ensure that your home is rebuilt even if the rebuild cost surpasses your limit — which is often the case for historic homes once labor and materials are factored in.

Water backup and service line coverages

Another important — but often overlooked — consideration has less to do with your home’s structure and more to do with what’s under it. These in-ground coverages for water backup and service lines could especially come in handy for those who live in older homes, which often have old or crumbling pipes and utility lines. The costs of fixing these can get exorbitantly expensive, as the responsibility of maintaining these lines falls on the homeowner.

How to lower your premium: tips and tricks for saving money on insurance

Homeowners insurance for an older home can get pricey — especially as your property ages beyond 30 years — but there are a few ways you can alleviate the cost. Here are our expert tips on lowering your insurance premium.

The replacement cost of your home significantly impacts your rate. Reevaluate your insurance needs by having your insurer assess your home’s replacement value every few years. Doing this will ensure that you’re not paying for coverage you don’t need.

Insurance premiums and deductibles carry an inverse relationship: the higher your deductible, the lower your premium. Accepting a larger share of financial responsibility means that your insurer will pay less if you need to file a claim.

Knowing what’s worth filing a claim for and what’s not will save you money, time and hassle in the future. Even having one recent claim on your record is a red flag to many insurance companies.

If you already have an auto insurance policy with one company, consider bundling it with your homeowners insurance. Bundling discounts are offered by most insurers. It’s a great way to easily save some money on your rate and deal with just one monthly invoice for your insurance needs.

Discounts vary from company to company. Whichever homeowners insurance company you choose, make sure to always inquire about discounts. Learn more about common discounts on homeowners insurance.

Zebra tip: Regular home maintenance lowers your risk of major repairs

Another option that may help lower home insurance premiums is by employing regular maintenance to your home and systems. Sturdier material, reinforced or updated systems, and routine checks on your home's ammenities strengthens the quality of your home and can save you in major repairs down the line.

If you’re still unhappy with how much you’re paying for coverage, don’t be afraid to switch companies. Enter your ZIP code below to find your best home insurance rate from insurance providers across the nation.

Make an informed decision: compare insurance rates today.

Frequently asked questions

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.