Homeowners Insurance for a New Construction Home

- New homes often cost less to insure because they meet modern building codes and have new materials, wiring, and roofs.

- Higher rebuild costs can raise coverage amounts, even if rates per dollar of coverage are lower.

![]() Why you can trust The Zebra

Why you can trust The Zebra

Kristine joined The Zebra in 2019 as an in-house content researcher and writer, with a property and casualty insurance license. Before joining The Ze…

- Licensed Insurance Agent — Property and Casualty

- 6+ years of Experience in the Insurance Industry

Jean Lucey has researched and written about insurance matters for well over 30 years. A current member of The Zebra's Insurance Expert Review Board, …

- CPCU, Chartered Property Casualty Underwriter

Ross joined The Zebra as a writer and researcher in 2019. He specialized in writing insurance content to help shoppers make informed decisions.

Ross h…

- 5+ years in the Insurance Industry

Homeowners insurance for new construction

Whether you’re a first-time homebuyer or a seasoned homeowner looking to upgrade to a newer home, your mortgage lender will require you to get home insurance for the new property. Homeowners insurance comprises some crucial coverages that will protect the dwelling’s structure, your personal property, liability and more.

If you’re in the process of closing on the property, now is the time to start shopping around for new home insurance to insure your investment — even if it’s still under construction. The good news is that insurance companies are partial to newly constructed homes, so they’re cheaper to insure than an older home. A new home construction discount is also a common offering by many companies and is often one of the biggest discounts you can get.

Consult our guide to finding insurance for a brand new house, and the best ways to save even more on your insurance rate.

Key takeaways

- New constructions are cheaper to insure than older homes, with an average cost of $80 per month

- Insurance companies favor insuring new homes because they have lower risk profiles

- Rates can go up by 53% once a house reaches 10 years of age

- The cheapest insurance company for a new construction is Progressive

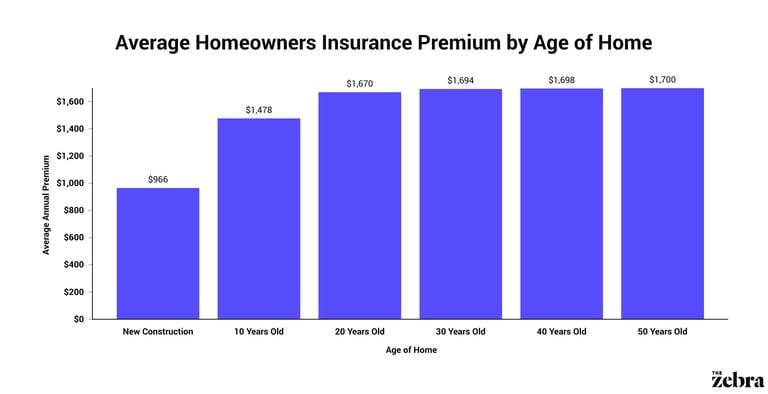

How much does home insurance cost for new constructions?

The newer the home, the cheaper it will be to insure. The price difference in insuring a new construction versus a 10-year-old house is 53%. Rates climb incrementally as the home ages beyond 30 years.

Compared to a home built in 1990, you can save more than $700 a year in insurance costs by opting for a new build. Learn more about our rate-gathering methodology.

| Age of Home | Average Annual Premium | Monthly Premium | % Difference |

|---|---|---|---|

| New Construction | $966 | $80 | - |

| 10 Years Old | $1,478 | $123 | +53% |

| 20 Years Old | $1,670 | $139 | +13% |

| 30 Years Old | $1,694 | $141 | +1% |

| 40 Years Old | $1,698 | $142 | +0.23% |

| 50 Years Old | $1,700 | $142 | +0.12% |

If you’re looking to buy a new construction home, you’re in luck; insurance companies favor covering new homes because everything is new — from foundation to roof — and thus, comes with lower risk profiles.

Insurers charge lower premiums for newly built homes since these properties are much less likely to suffer from issues that tend to afflict older homes; things like faulty wiring and crumbling roofs are more likely to cause damage that would warrant insurance involvement. Apart from weather-related claims, insurance companies don’t anticipate the owner of a brand new home will need to file a property claim anytime soon.

The Zebra’s homeowners insurance data methodology

The Zebra’s Dynamic Insurance Rating Tool for home and auto insurance rates utilizes the latest ZIP code-level rate filings from across the U.S., sourced from Quadrant Information Services and S&P Global. These filings, typically updated annually or biennially by insurers, are verified through Quadrant’s QA process and then integrated into The Zebra’s estimator.

The displayed rates are based on a dynamic home and auto profile designed to reflect the content of the page. This profile is tailored to match specific factors such as age, location, and coverage level, which are adjusted based on the page content to show how these variables can impact premiums.

For a comprehensive understanding, see our detailed methodology.

New construction home insurance rates by company

When your home was built is a relatively small piece of the pie when companies calculate insurance quotes, but it remains a factor nonetheless. On average, you can expect to pay $80 per month to insure a new build.

See more in the table below to see a breakdown of rates by home insurance company and the age of the home.

The cheapest company for a new build home was Progressive, with an average monthly payment of just $44 — $36 less than the national average.

| Insurance Company | New Construction | 10 Years Old | 20 Years Old | 30 Years Old | 40 Years Old | 50 Years Old |

|---|---|---|---|---|---|---|

| Allstate | $1,033 | $1,594 | $1,709 | $1,755 | $1,750 | $1,759 |

| American Family | $1,422 | $2,261 | $2,396 | $2,405 | $2,409 | $2,422 |

| Amica | $772 | $1,089 | $1,145 | $1,152 | $1,152 | $1,144 |

| Farmers | $1,093 | $1,455 | $1,606 | $1,553 | $1,539 | $1,516 |

| Nationwide | $693 | $1,236 | $1,447 | $1,487 | $1,524 | $1,542 |

| Progressive | $533 | $1,355 | $1,913 | $1,941 | $1,884 | $1,810 |

| State Farm | $885 | $1,356 | $1,520 | $1,524 | $1,531 | $1,532 |

| Travelers | $929 | $1,444 | $1,671 | $1,716 | $1,703 | $1,692 |

| USAA | $706 | $1,231 | $1,477 | $1,484 | $1,495 | $1,475 |

Find out who the cheapest home insurer is for your new construction by entering your ZIP code below to get quotes and compare them side-by-side.

Compare quotes to find the most affordable rate for your new home.

Builders risk insurance: home building insurance for homes under construction

If your new abode is being freshly built for you, there’s an additional consideration to be mindful of — protecting your property while it’s under construction.

A standard homeowners insurance policy may exclude coverage for damages incurred while the home is being built. Consult your insurance agent to verify whether or not your policy offers coverage under these circumstances.

Construction sites can be prone to perils like vandalism, theft and accidental damage, so your insurance company could require that you add builders risk insurance (also known as course of construction insurance) as a policy add-on to cover your dwelling under construction or if you’re embarking on a major construction project or remodel.

A builders risk policy offers much less coverage than a typical homeowners policy as it’s intended to be temporary. It does not include coverage for:

- Liability protection (this could be covered if your general contractor or builder carries insurance, which includes general liability coverage in case of injuries and/or property damage)

- Personal property

- Additional living expenses

- Medical payments to others

Once the new house is completed, reassess the home’s replacement cost and update your insurance coverage to a standard policy. Learn more about what home insurance covers.

The best ways to save on home insurance

One of the best ways to avoid overpaying is to shop for a new policy regularly, and don't be afraid to make the switch if another home insurance company is offering a cheaper deal. Even with discounts, there's a chance you can get a lower insurance premium elsewhere as some insurers are just more expensive than others — however, you'll need to make sure you're not getting worse coverage options in exchange for a cheaper homeowners insurance quote. See below for more expert tips on how to save.

A bundling discount is one of the more common discounts that can be found at most insurance companies. Already have auto insurance? Look into bundling home insurance and car insurance with the same insurer to save about $268 per year, on average.

The number of discounts varies from company to company, and sometimes it may be built into your rate when you shop around for quotes. While home insurance discounts tend to be quite small, they can add up. Here are some common discounts for homeowners insurance:

- Multi-policy and bundling

- New home construction or homebuyer

- Payments: Paperless, pay in full, EFT, automatic

- Claims-free

- Senior or mature homeowners

- Roof upgrade

- Home security and fire prevention system

- Smoke-free

As long as you’re comfortable paying a higher deductible (for homeowners insurance, this could be well into thousands of dollars) in the event of a covered loss, this is an easy way to lower your rate. Premiums and deductibles work inversely — raising one will lower the other, and vice versa.

Not every incident is worth filing a claim for, and it could be harder to find an insurance company willing to provide coverage if you have a history of losses. All property claims are tracked in a national database called the Comprehensive Loss Underwriting Exchange (CLUE) that insurance companies can access. In general, you should file a claim if repair or replacement costs exceed the deductible you’ll pay. Learn more about when to file a homeowners insurance claim.

Ready to see how much you can save? Use our comparison tool to compare rates from local and national homeowners insurance companies side-by-side.

Compare home insurance quotes quickly and easily.

FAQs

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.