Car Insurance for Renters

- Bundling your renters and auto insurance is a simple way to streamline your coverage, and it often comes with a nice discount.

- Be sure to compare the total cost, not just the discount percentage, when you’re shopping around.

![]() Why you can trust The Zebra

Why you can trust The Zebra

Ava joined The Zebra in 2016 as a licensed insurance agent and writer. She now serves as director of insurance content, leading coverage strategy and…

- 9+ years of Experience in the Insurance Industry

Beth joined The Zebra in 2022 as an Associate Content Strategist. A licensed insurance agent, she specializes in creating clear, accessible content t…

- Licensed Insurance Agent — Property and Casualty

- Associate in Insurance (AINS)

- Professional Risk Consultant (PRC)

- Associate in Insurance Services (AIS)

Renata joined The Zebra in 2020 as a Customer Experience Agent. Since 2021, she has worked as a licensed insurance professional and content strategis…

- Licensed Insurance Agent — Property and Casualty

- 5 years of experience in the insurance industry

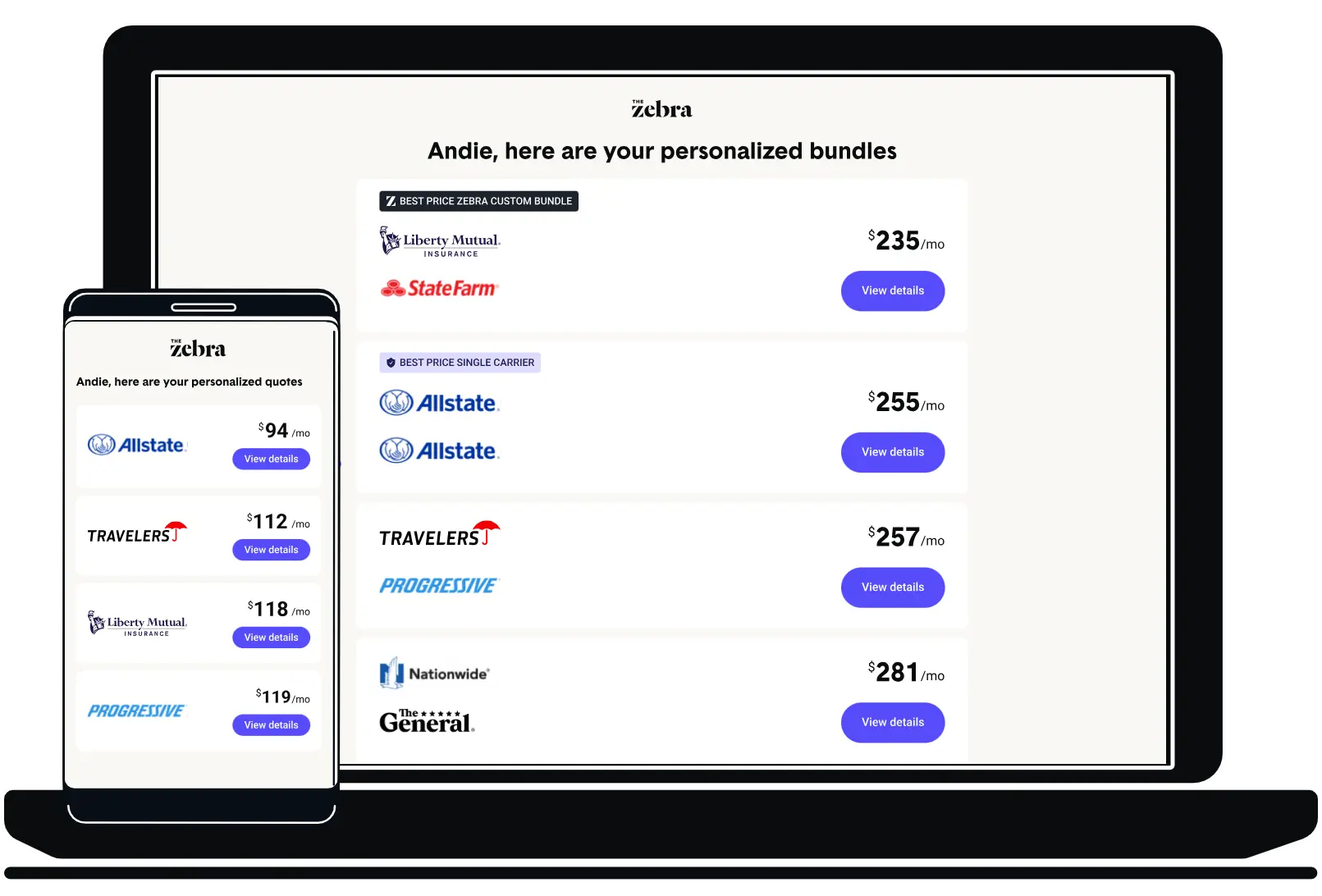

The best cheap auto and renters insurance quotes in 2026

The Zebra analyzed millions of rates from top insurance companies to find the best deals for renters and auto insurance bundles in 2026. Below, find our top picks for the cheapest bundled rates from trusted and well-known providers. Keep reading to explore discounts and rates from more top insurers.

Best Company Overall

State Farm ranked best overall, while USAA, limited to military members and their families, scored equally high.

Cheapest Bundle

Erie Insurance had the cheapest average price for renters shopping for auto insurance.

Largest Bundling Discount

Though Liberty Mutual wasn’t the cheapest overall, it offered the largest bundling discount at 10% savings.

Let The Zebra compare auto and renters quotes for you!

The 10 cheapest companies for auto and renters bundles

There are hundreds of insurance companies in the U.S., but for wide accessibility, we focused on carriers that provide renters and auto insurance bundles in most states. Travelers and USAA offer some of the cheapest bundled rates among these providers.

Note: This isn’t a renters-and-car insurance quote — the prices and discounts below apply only to auto insurance quotes with a renters insurance bundling discount.

| Company | 6-Month Rate with Bundling Discount | % Savings |

|---|---|---|

| Erie | $419 | 2% |

| USAA | $539 | 1% |

| GEICO | $588 | 2% |

| State Farm | $605 | 7% |

| American Family | $627 | 8% |

| Nationwide | $664 | 8% |

| Farmers | $762 | 8% |

| Progressive | $764 | 6% |

| Liberty Mutual | $784 | 10% |

| Allstate | $962 | 5% |

The Zebra’s auto insurance data methodology

The Zebra’s Dynamic Insurance Rating Tool for home and auto insurance rates utilizes the latest ZIP code-level rate filings from across the U.S., sourced from Quadrant Information Services and S&P Global. These filings, typically updated annually or biennially by insurers, are verified through Quadrant’s QA process and then integrated into The Zebra’s estimator.

The displayed rates are based on a dynamic home and auto profile designed to reflect the content of the page. This profile is tailored to match specific factors such as age, location, and coverage level, which are adjusted based on the page content to show how these variables can impact premiums.

For a comprehensive understanding, see our detailed methodology.

40% of customers reported switching carriers specifically to bundle their policies, but this is only a good idea if the math lines up.[1] For example, a 10% bundling discount on a $500 premium ($450 total) still costs more than a $425 quote with no discount.

Similarly, one company might be cheaper for renters insurance but more expensive for auto insurance. This is because companies price each line of insurance differently based on their unique risk models.

The best car insurance companies for renters

The Zebra surveyed customers on online experience, claims satisfaction, ease of use, customer service, trust, and willingness to recommend.[2] Renters rated USAA as the top auto carrier, excelling in every category. State Farm and Nationwide also performed well, ranking in the top five for trust, customer service, ease of use, and online satisfaction.

Best for Military

USAA tied with State Farm at 4.6/5 but is limited to military members and their families.

Best for Most Renters

State Farm tied with USAA with a 4.6/5, making it a great choice for most renters looking to bundle.

Runner-Up

Nationwide came in a close second with a respectable score of 4.4/5.

Sometimes, paying a bit more means better service, smoother claims, and fewer headaches. The “best” bundle isn’t just about cost—it’s about value.

How to decide if bundling is right for you

Bundling your auto and renters insurance can save you money and simplify your policies—but not always. Here's how to decide if bundling is right for you:

The company that has the best auto insurance rate might not necessarily have the best renters insurance rate, even with a hefty bundling discount.

Insider tip: Our Head of Agency, Katie Gold, encourages going line by line when comparing policies: "A lot of people focus only on the cost of insurance without truly comparing coverage apples to apples....Often, you’ll discover that certain coverages were removed, limits were lowered, or deductibles were increased. It’s essential to ensure all coverages are equal first, and then compare the price."

Ensure the bundled package doesn’t limit your coverage needs or force compromises. For example, a bundle might offer great auto coverage but limit renters insurance to lower property limits or exclude protections of certain valuables.

Some providers offer other discounts—like good driver or claims-free discounts—that can also affect the final price you pay for coverage.

Make sure the provider offering the bundle has strong customer service and claims satisfaction ratings. Read our reviews of insurance companies.

Some insurers use subsidiaries for certain lines of insurance, especially renters and homeowners. For example, your auto insurance might be handled by the parent company, while renters insurance is managed by a subsidiary with separate claims processes, customer service teams, or coverage options.

It's important to understand which company handles each part of your bundle and review their individual coverage terms and service ratings.

When to bundle auto and renters insurance

-

The total cost bundled is less than the total cost of both policies bought from separate companies.

-

Both policies' coverage options meet your needs.

-

You prioritize convenience and have confirmed bundling won’t result in separate bills or claims processes from a subsidiary.

-

The insurer (and, if relevant, their subsidiary) has good customer service and claims satisfaction ratings.

-

Having policies with two different companies has a cheaper total cost

-

The bundled policies don’t fully meet your coverage needs or force compromises.

-

Renters coverage is provided through a subsidiary with a weaker reputation.

-

Convenience is your priority and the company only offers renters insurance through a subsidiary that requires separate bills, claims processes, and service teams.

Need help comparing rates?

Figuring out if bundling is the right choice can be tricky, but you don’t have to do it alone. Our licensed insurance agents can help you:

- Compare Your Options and Maximize Your Savings: We’ll break down bundled and standalone policies from multiple insurers to find the best value for your needs.

- Tailor Your Coverage: Ensure your policies meet your unique needs.

- Save Time and Stress: Skip the guesswork and let us help you make an informed, fast, and hassle-free decision.

Speak with The Zebra's licensed in-house agents or compare auto insurance rates using The Zebra's free tool below.

Here at The Zebra, we do the searching, you do the saving.

FAQs about bundling auto and renters insurance

-

Monthly user surveys via the Marble App. The Zebra

Monthly user surveys via the Marble App. The Zebra

-

2024 Customer Satisfaction Survey. The Zebra

2024 Customer Satisfaction Survey. The Zebra

-

Data Methodology. The Zebra’s Dynamic Insurance Rating Tool

Data Methodology. The Zebra’s Dynamic Insurance Rating Tool

About The Zebra

The Zebra is not an insurance company. We publish data-backed, expert-reviewed resources to help consumers make more informed insurance decisions.

- The Zebra’s insurance content is written and reviewed for accuracy by licensed insurance agents.

- The Zebra’s insurance editorial content is not subject to review or alteration by insurance companies or partners.

- The Zebra’s editorial team operates independently of the company’s partnerships and commercialization interests, publishing unbiased information for consumer benefit.

- The auto insurance rates published on The Zebra’s pages are based on a comprehensive analysis of car insurance pricing data, evaluating more than 83 million insurance rates from across the United States.